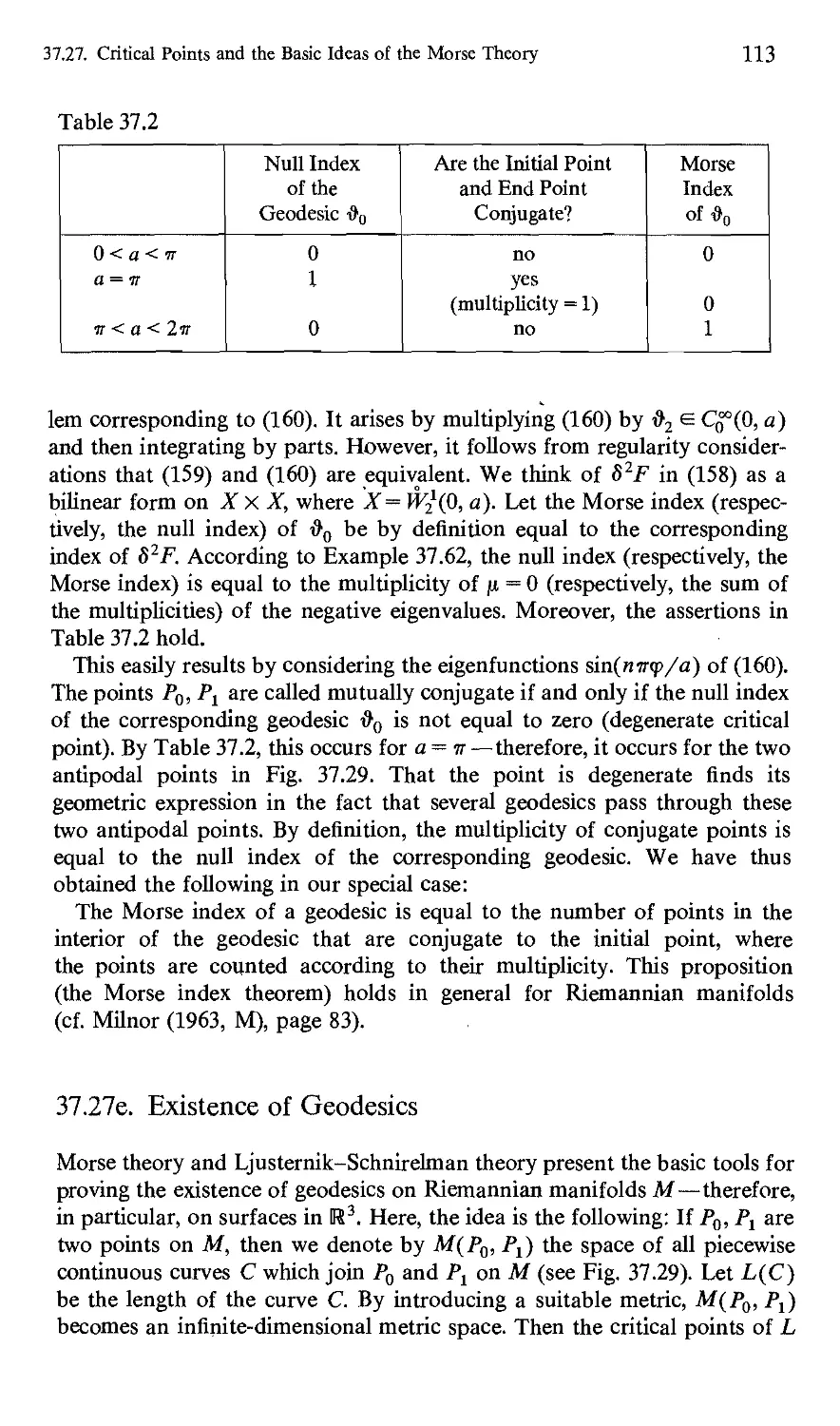

/

Author: Zeidler E.

Tags: mathematics mathematical physics nonlinear functional analysis variational methods

Year: 1984

Similar

Text

Eberhard Zeidler

Nonlinear

Functional Analysis

and its Applications

Variational Methods

and Optimization

S& BBBb'I

Leonhard Euler (1707-1783)

Eberhard Zeidler

Nonlinear

Functional ^lalys]

and its Applieatioi

III: Variational Methods

and Optimization

Translated by Leo F. Boron

With 111 Illustrations

Gl

Eberhard Zeidler

Sektion Mathematik

Karl-Marx-Platz

7010 Leipzig

German Democratic Republic

Leo F. Boron (Translator)

Department of Mathematics

and Applied Statistics

University of Idaho

Moscow, ID 83843

U.S.A.

AMS Classification: 58-01, 58-CXX, 58-EXX

Library of Congress Cataloging in Publication Data

Zeidler, Eberhard.

Nonlinear functional analysis and its applications.

Bibliography: p.

Includes index.

Contents: —pt. 3. Variational methods and

optimization.

1. Nonlinear functional analysis—Addresses, essays,

lectures. I. Title.

QA321.5.Z4513 1984 515.7 83-20455

© 1985 by Springer-Verlag New York Inc.

All rights reserved. No part of this book may be translated or reproduced in

any form without written permission from Springer-Verlag, 175 Fifth Avenue,

New York, New York 10010, U.S.A.

Typeset by Science Typographers, Inc., Medford, New York.

Printed and bound by R. R. Donnelley & Sons, Harrisonburg, Virginia.

Printed in the United States of America.

987654321

Dedicated in gratitude to my teacher

Professor Herbert Beckert

Preface

As long as a branch of knowledge offers an abundance of problems, it is full

of vitality.

David Hilbert

Over the last 15 years I have given lectures on a variety of problems in

nonUnear functional analysis and its appUcations. In doing this, I have

recommended to my students a number of excellent monographs devoted to

specialized topics, but there was no complete survey-type exposition of

nonUnear functional analysis making available a quick survey to the wide

range of readers including mathematicians, natural scientists, and engineers

who have only an elementary knowledge of linear functional analysis. I have

tried to close this gap with my five-part lecture notes, the first three parts of

which have been pubUshed in the Teubner-Texte series by Teubner-Verlag,

Leipzig, 1976, 1977, and 1978. The present EngUsh edition was translated

from a completely rewritten manuscript which is significantly longer than

the original version in the Teubner-Texte series. The material is organized in

the following way:

Part I: Fixed Point Theorems.

Part II: Monotone Operators.

Part III: Variational Methods and Optimization.

Parts IV/V: Applications to Mathematical Physics.

The exposition is guided by the following considerations:

(a) What are the supporting basic ideas and what intrinsic interrelations

exist between them?

(/6) In what relation do the basic ideas stand to the known propositions of

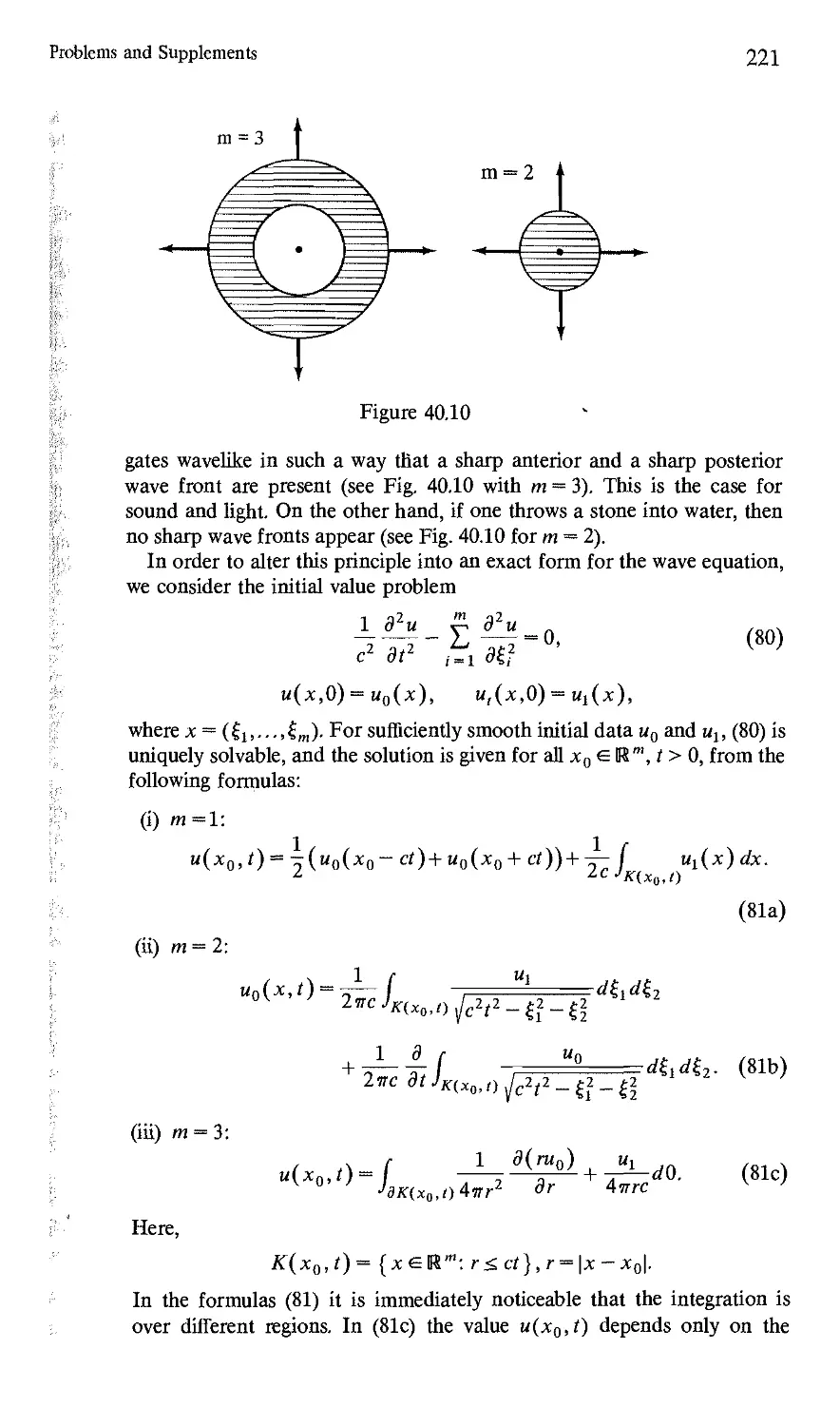

classical analysis and Unear functional analysis?

(•y) What typical applications are there?

Vll

Vlll

Preface

Special emphasis is placed on motivation. The reader should always have

the feeling that the theory is not developed for its own sake but rather for

the effective solution of concrete problems. At the same time I try to outline

a variegated picture of the subject matter which ranges from the

fundamental questions of set theory (the Bourbaki-Kneser fixed point theorem) to

concrete numerical methods, encompassing numerous applications to

physics, chemistry, biology, and economics. The reader should see

mathematics as a unified whole, with no separation between pure and applied

mathematics. At the same time we show how deep mathematical tools can

be used in the natural sciences, engineering, and economics. The

development of nonlinear functional analysis has been influenced in an essential

way by complicated natural scientific questions; the close contact with the

natural sciences and other sciences will also be of great significance for the

development of nonlinear functional analysis. In our exposition, the use of

analytic tools stands in the foreground, but we also seek to show

connections with algebraic and differential topology. For instance, Sections 37.27

and 37.28 contain an introduction to Morse theory as well as to singularity

and catastrophe theory. To reach the largest possible readership and to

fashion a self-contained exposition, important tools from linear functional

analysis are provided in the appendices to Parts I and II. These are

presented so that readers with a skimpy background can familiarize

themselves with this material. We forego, at the outset, the greatest possible

generality, but rather seek to expose the simple intrinsic nucleus without

trivializing it. According to the author's experience, it is easier for the

student to generalize familiar mathematical ideas to a more general situation

than to elicit the basic idea from a theorem that is formulated very generally

and burdened with many technical details. The teacher must help him in

that task. In order to make it easier for the reader to grasp the central

results, a number of propositions have been listed in a separate section

called List of Theorems to be found on page 643. It is clear that this

procedure is not entirely free of arbitrariness. However, we hope that the

lists of Theorems for Parts I-V provide an overview of the essential

substance of nonlinear functional analysis. Furthermore, since, in the

experience of the author, it is frequently difficult, because of a flood of details,

for the student to recognize the interrelationships between different

questions and the general strategies for the solution of problems, special

emphasis is placed on these interrelationships.

We have given a general overview of the content of Parts I-V and the

basic idea of nonlinear functional analysis in the Preface and in the

introduction to Part I. The present Part III consists of the following topics:

(a) Introduction to the subject.

(fi) Two fundamental existence and uniqueness principles.

(•y) Extremal problems without side conditions.

(8) Extremal problems with smooth side conditions.

(e) Extremal problems with general side conditions.

Preface

IX

(f) Saddle points and duality,

(rj) Variational inequalities.

In the introduction, and in the schematic survey in Fig. 37.1 on page 3, we

give an overview of the interrelationships between various extremal

problems. In the comprehensive introductory Chapter 37, we present many

simple, but typical, examples that are representative of those concrete

problems that have played a central role in the historical development of the

subject. In order to obtain an impression of the extraordinary variety of

problems involved, the reader should glance at the list of subjects for

Chapter 37 that appears in the Contents. In the immediately following

chapters it is our chief concern to show the reader that these problems can

be handled with the aid of a unified theory of extremal problems. The

essence of this unified theory consists of a small number of fundamental

principles of functional analysis. The title of Part III, Variational Methods

and Optimization, indicates-that we consider aspects of the classical calculus

of variations as well as modern optimization theory and their

interrelationships. By working out the supporting ideas and general fundamental

principles, we also wish to help the reader obtain an understanding of the

substance of the extraordinarily comprehensive and turbulently

accumulating literature on extremal problems, to classify these works according to

their ideas, and to note the emergence of new ideas.

Each of the 21 chapters is self-contained. Each begins with motivations,

heuristic considerations, and indications of the typical problems to be

investigated and contains the most important theorems and definitions

together with elucidating examples, figures, and typical applications. We

also do not shun citing very simple examples in the interest of the reader.

Furthermore, we always try to penetrate as quickly as possible to the heart

of the matter. We try to achieve the situation where the reader knows at

each phase of the book what concrete applications the general

considerations allow. In general, a very careful selection of the material had to be

made because one could write each chapter as a special monograph and, to

some extent, such monographs already exist. Here, we describe the

applications to nonlinear differential and integral equations, differential

inequalities, one-dimensional and multidimensional variational problems, linear and

convex optimization problems, problems in approximation theory and game

theory, continuous and discrete control problems for ordinary and partial

differential equations, and also consider important approximation methods.

In particular, in Section 37.29, we explain the basic ideas of 10 important

methods and principles for the construction of approximation methods. In

the introduction to Part I we have already pointed out that in numerical

methods the devil rides high on detail. However, general principles and

theoretical investigations of approximation methods within the setting of

numerical functional analysis are useful for recognizing the basic ideas and

for arranging the abundance of concrete numerical methods into a unified

point of view. We examine a number of more profound applications of

nonlinear functional analysis to mathematical physics in Parts IV and V.

X

Preface

At the end of each chapter the reader will find problems and references to

the literature. The problems vary considerably in their degree of difficulty:

(a) Problems without asterisks serve as drills in the material presented and

require no additional tools.

(j8) Problems with asterisks are more difficult—additional ideas are

required to solve them.

(•y) Problems with double asterisks are very difficult—one needs substantial

additional information to solve them.

Each problem contains either a solution or a precise reference to the

monograph or original work in which the solution can be found. Moreover,

we try to clarify the meaning of the results with explanatory remarks. The

problems with one or two asterisks are in part so devised that they present

targeted references to the literature on important extensions of results or

they serve to extend the reader's mathematical horizon. A number of topics

will be treated supplementarily in the problem collections. These topics are

particularly extensive in Chapter 40, where we try to sketch for the reader a

line of development from the classical calculus of variations and from

geometrical optics up to the modern theory of Fourier integral operators. In

this we let ourselves be led by the experience that the penetration of a

complicated theory is made easier for the student when she/he has an

ultimate goal from the beginning and knows the connection between the

goal and the simpler questions familiar to her/him.

The references to the literature at the end of each chapter are styled as

follows: Krasnoselskii (1956, M, B, H), etc. The year refers to the list of

literature at the end of the book. Furthermore, the capital Latin letters

mean:

M: monograph;

L: lecture notes;

S: survey;

P: proceedings;

B: the cited work contains a comprehensive bibliography;

H: the cited work contains references to the historical development of the

subject.

In this connection, the references to the literature are at the same time

supplied with clarifying captions which explain the interrelationship

between the works cited. On page 166 one finds "Recent trends". From the

abundance of available literature we have made a careful but necessarily

subjectively biased selection, which in the author's opinion will easily afford

the reader as comprehensive a picture as possible concerning the

farther-leading results. In this, the emphasis lies naturally on the surveys

and monographs. However, we also cite a number of classical works which

were of special significance for the development of the subject. We

recommend that the reader glance at several of these works in order to obtain ah

Pref.

XI

active impression of the genesis of new results and of the historical

development of mathematics. Unfortunately, in order to keep the list of literature

within tolerable bounds, we had to forego listing many important

references.

In the choice of the presentation it was taken into consideration that in

general no book is read completely from beginning to end. We hope that

even a quick skimming of the text will suffice for one to grasp the essential

contents. To this end, we recommend reading the introductions to the

individual chapters, the definitions, the theorems (without proofs), and the

examples (without proofs) as well as the comments in the text between these

definitions, theorems, etc., which point out the meaning of the individual

results. The reader who does not have time to solve the problems should,

however, briefly scrutinize the captions to the problems and the adjoining

remarks, which elucidate the meaning of the formulation of the problems

and the interrelationships." The reader who is interested in supplementary

problem material can try to prove independently all of the examples in the

text without referring to the given proof. Moreover, in the references to the

literature in Section 37.29, books are cited in which the reader will find

comprehensive collections of exercises that as a rule are not too difficult. All

hypotheses both in the theorems and in the examples are explicitly stated so

that the reader avoids a time-consuming search for the assumptions in the

antecedent text. We have taken pains to reduce the number of definitions to

a minimum in order not to burden the reader with too many concepts. On

page xii one finds a list of the most important definitions. In order to clarify

interrelationships, several assertions that belong together are at times

combined into a single theorem. In this form of exposition, we have also kept in

mind the natural scientist and the engineer who want primarily to gain

information on which mathematical tools are available for the various

nonlinear problems. We recommend Chapter 37 to the reader who wishes to

examine the class of problems which the general theory allows one to treat.

However, it suffices to glance at this comprehensive chapter, because

references will later be made at the appropriate places. The reader whose

priority is to become acquainted with the theoretical framework can

immediately begin with Chapter 38 and, on first reading, omit the sections in

the individual chapters that are devoted to applications.

Grasping the individual steps in the proofs as well as the essential ideas of

the proofs is made easier by the careful organization of the proofs. It is a

truism that only by a precise study of the proofs one can penetrate more

deeply into a mathematical theory.

Part III is to a large extent independent of the other parts. However,

where necessary, we do refer to particular results of the other parts. Note

that several auxiliary tools are made available in Parts I and II (basic

information concerning linear functional analysis, Sobolev spaces, etc.). We

formulate a number of results for locally convex spaces. The reader who is

not familiar with this material can orient himself by reading the appendix to

Part I or replace the concept of a locally convex space by that of a Banach

Xll

Preface

or Hilbert space. Dual pairs are important for duality theory. We explain

this concept in the appendix to Part III. The reference Aj (20) relates to (20)

in the appendix to the ith part. (37.20) is formula (20) in Chapter 37.

Within a particular chapter, we forego giving the chapter number of the

equation. In each chapter, theorems are distinguished by capital letters, so

that, for instance, "Theorem 57.B in Section 57.5" means the second

theorem in Chapter 57, located in Section 5 of that chapter. Propositions,

lemmas, corollaries, definitions, remarks, conventions, counterexamples,

standard examples, and examples are numbered consecutively in each

chapter—for example, in Chapter 41 one finds Definition 41.1, Proposition

41.2, Corollary 41.3, etc., in that order. The end of a proof is indicated by

the symbol □. We subdivide the chapters among the five separate parts of

this work in the following way:

Part I: Chapters 1-17.

Part II: Chapters 18-36.

Part III: Chapters 37-57.

Part IV: Chapters 58-79.

Part V: Chapters 80-100.

A list of symbols used can be found on page 637. We have taken pains to

employ the notation that is generally used. To avoid confusion, we point out

several peculiarities at the beginning of the list of symbols on page 637. A

detailed subject index can be found on page 651. As far as abbreviations are

concerned, we use only B-space (respectively, H-space) for Banach space

(respectively, Hilbert space), F-derivative (respectively, G-derivative) for

Frechet derivative (respectively Gateaux derivative) as well as M-S

sequence for Moore-Smith sequence and L-S deformation for

Ljusternik-Schnirelman deformation.

I have taken pains to write as interesting and diverse a book as possible.

Of course, whether or not I have succeeded in this only the reader can

decide.

I am indebted to numerous colleagues for interesting conversations and

letters as well as for sending me articles and books—I thank them all

heartily. I am especially grateful to my mentor Professor Herbert Beckert

for all that I learned from him as a scientist and as a human being. I should

like to dedicate the present volume to him. I cordially thank Paul H.

Rabinowitz and the Department of Mathematics of the University of

Wisconsin, Madison, for the invitation as guest resident scholar during the

fall semester 1978. The very stimulating atmosphere in Madison influenced

the final form of the exposition in an essential way. In the tasks of typing

the manuscript and of making copies, I was supported in an amiable way by

a number of colleagues, both male and female. I should like to very heartily

thank Ursula Abraham, Sonja Bruchholz, Elvira Krakowitzki, Heidi Kilhn,

Hiltraud Lehmann, Karin Quasthoff, Werner Berndt, and Rainer Schumann.

I would especially like to thank Rainer Schumann for a critical perusal of

parts of the manuscript. The understanding and extensive support shown to

Preface

xin

me by the librarian of our institute, Frau Ina Letzel, was of great value to

me. Furthermore, I thank the administrators of the Mathematics Section

of the Karl Marx University, Leipzig, and its director, Professor Horst

Schumann, for supporting this project.

I would also like to thank the translator, Professor Leo F. Boron,

University of Idaho, Moscow, for his excellent work. I am very indebted to

him for valuable suggestions and remarks. Finally, my special thanks go to

Springer-Verlag for the harmonious collaboration and the understanding

approach to all my wishes.

Eberhard Zeidler

Leipzig

Spring 1984

Contents

Introduction to the Subject 1

General Basic Ideas 4

CHAPTER 37

Introductory Typical Examples 12

§37.1. Real Functions in R1 13

§37.2. Convex Functions in R1 15

§37.3. Reai Functions in R N, Lagrange Multipliers, Saddle Points, and

Critical Points 16

§37.4. One-Dimensional Classical Variational Problems and Ordinary

Differential Equations, Legendre Transformations, the

Hamilton-Jacobi Differential Equation, and the Classical

Maximum Principle 20

§37.5. Multidimensional Classical Variational Problems and Elliptic

Partial Differential Equations 41

§37.6. Eigenvalue Problems for Elliptic Differential Equations and

Lagrange Multipliers 43

§37.7. Differential Inequalities and Variational Inequalities 44

§37.8. Game Theory and Saddle Points, Nash Equilibrium Points and

Pareto Optimization 47

§37.9. Duality between the Methods of Ritz and Trefftz, Two-Sided

Error Estimates 50

§37.10. Linear Optimization in R N, Lagrange Multipliers, and Duality 51

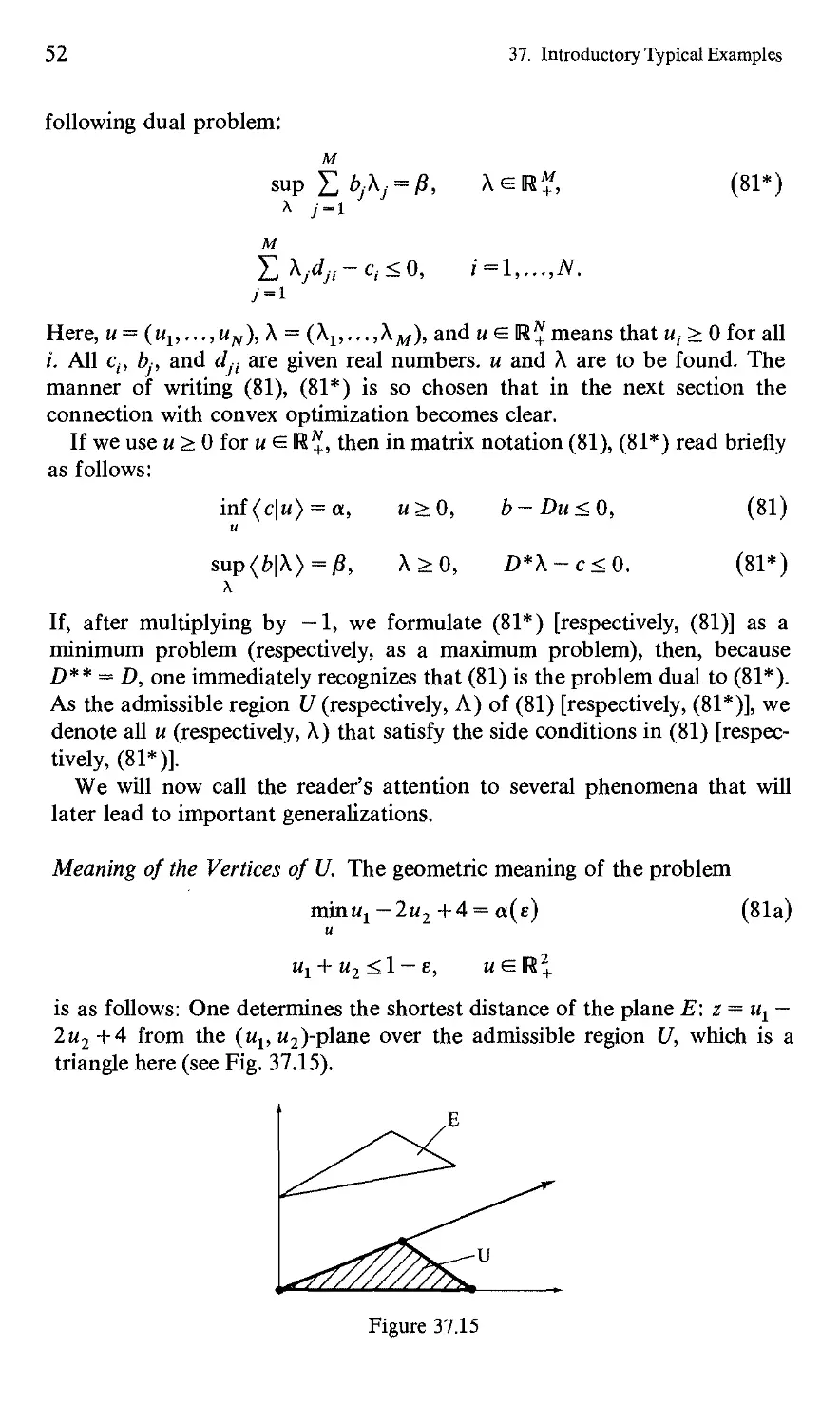

§37.11. Convex Optimization and Kuhn-Tucker Theory 55

§37.12. Approximation Theory, the Least-Squares Method, Deterministic

and Stochastic Compensation Analysis 58

§37.13. Approximation Theory and Control Problems 64

xvi

Contents

§37.14, Pseudoinverses, Ill-Posed Problems and Tihonov Regularization 65

§37,15. Parameter Identification 71

§37.16. Chebyshev Approximation and Rational Approximation 73

§37,17. Linear Optimization in Infinite-Dimensional Spaces, Chebyshev

Approximation, and Approximate Solutions for Partial

Differential Equations 76

§37.18, Splines and Finite Elements 79

§37.19. Optimal Quadrature Formulas 80

§37.20, Control Problems, Dynamic Optimization, and the Bellman

Optimization Principle 84

§37.21. Control Problems, the Pontrjagin Maximum Principle, and the

Bang-Bang Principle 89

§37.22, The Synthesis Problem for Optimal Control 92

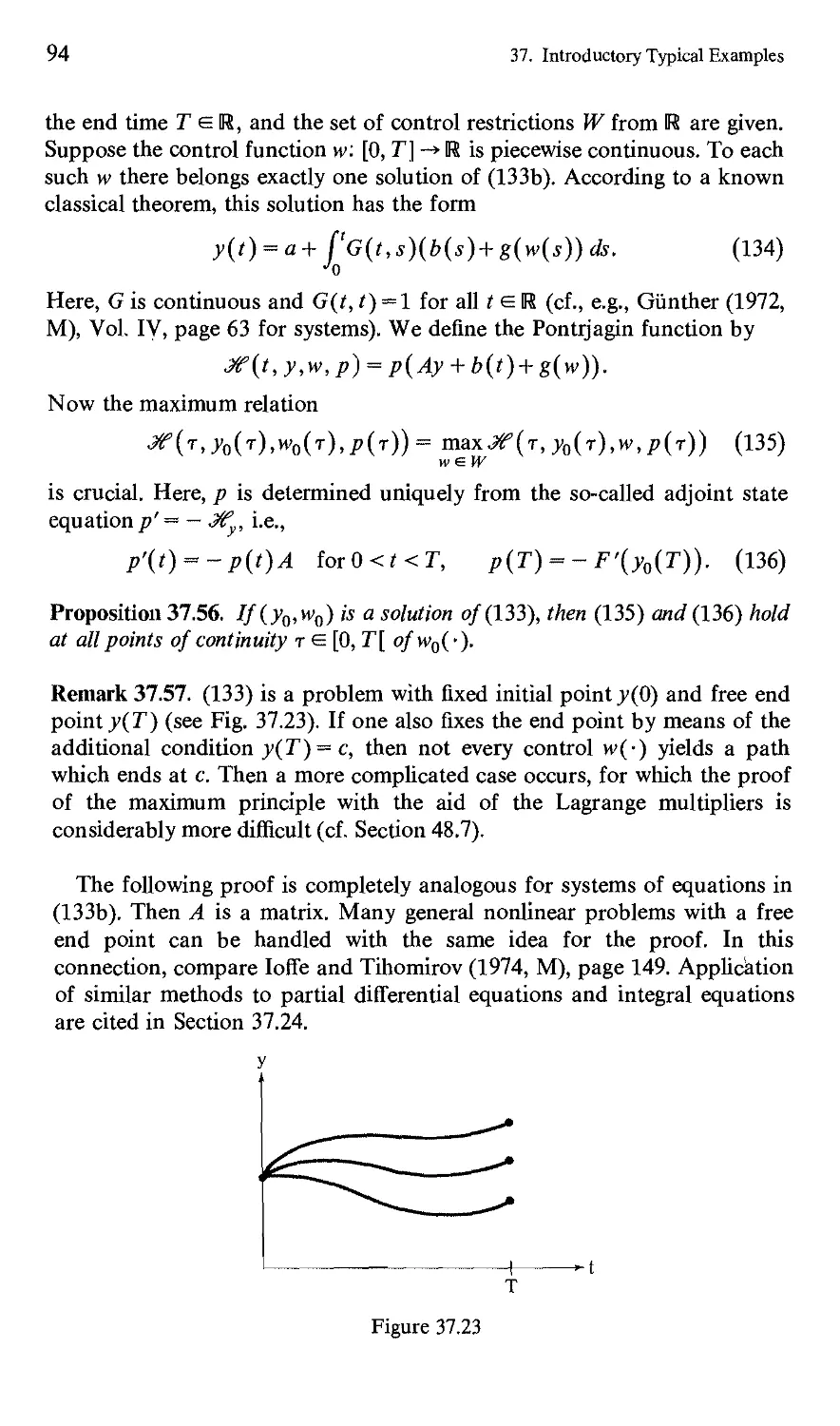

§37.23, Elementary Provable Special Case of the Pontrjagin Maximum

Principle 93

§37.24. Control with the Aid of Partial Differential Equations 96

§37.25. Extremal Problems with Stochastic Influences 97

§37.26. The Courant Maximum-Minimum Principle, Eigenvalues,

Critical Points, and the Basic Ideas of the Ljusternik-Schnirelman

Theory 102

§37,27. Critical Points and the Basic Ideas of the Morse Theory 105

§37.28. Singularities and Catastrophe Theory 115

§37.29. Basic Ideas for the Construction of Approximate Methods for

Extremal Problems 132

TWO FUNDAMENTAL EXISTENCE AND UNIQUENESS

PRINCIPLES

CHAPTER 38

Compactness and Extremal Principles 145

§38,1, Weak Convergence and Weak* Convergence 147

§38.2. Sequential Lower Semicontinuous and Lower Semicontinuous

Functionals 149

§38.3. Main Theorem for Extremal Problems 151

§38.4. Strict Convexity and Uniqueness 152

§38.5. Variants of the Main Theorem 153

§38.6, Application to Quadratic Variational Problems 155

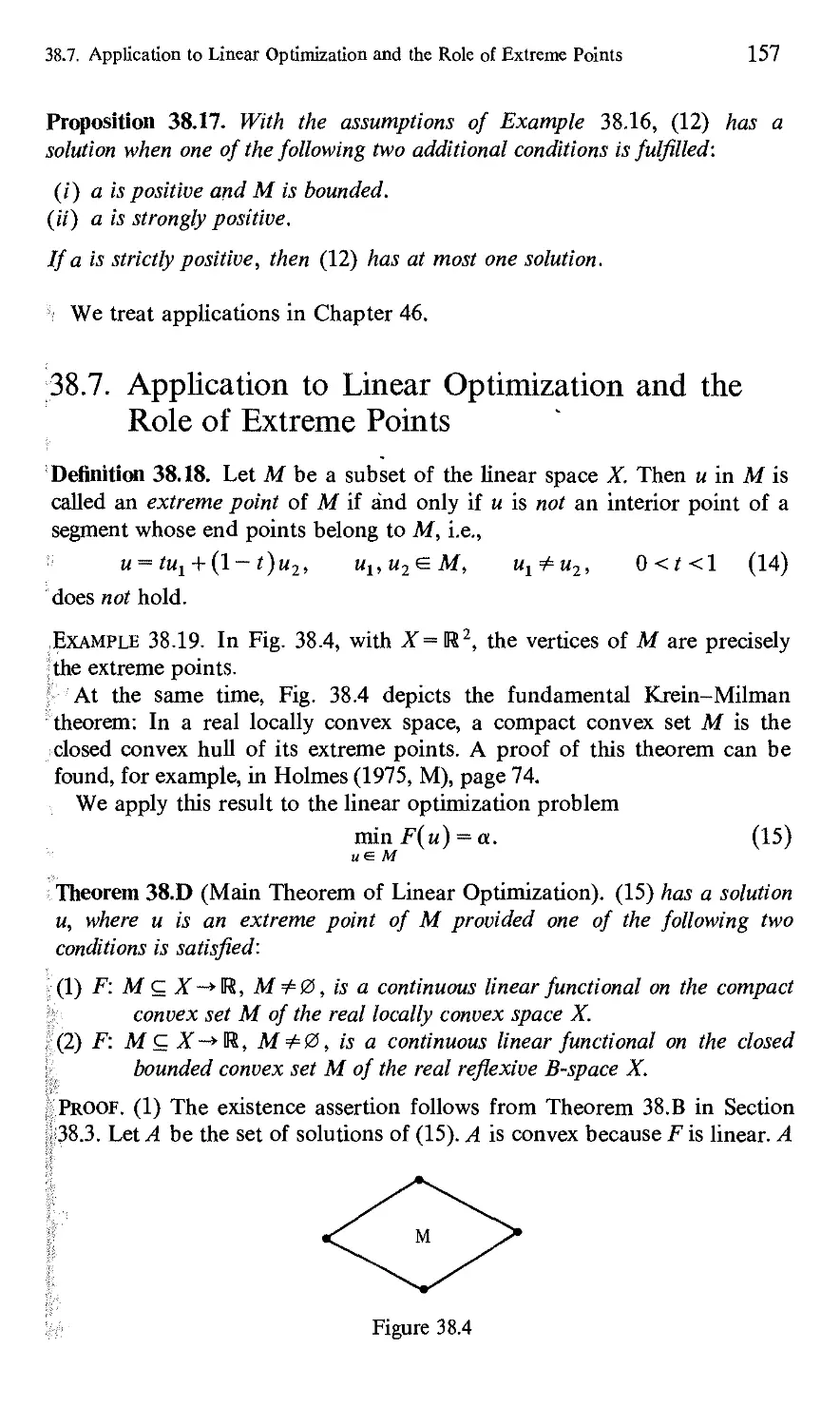

§38.7. Application to Linear Optimization and the Role of Extreme

Points 157

§38.8. Quasisolutions of Minimum Problems 158

§38,9. Application to a Fixed-Point Theorem 161

§38.10, The Palais-Smale Condition and a General Minimum Principle 161

§38.11. The Abstract Entropy Principle 163

Contents

XV11

CHAPTER 39

Convexity and Extremal Principles 168

§39.1. The Fundamental Principle of Geometric Functional Analysis 170

§39.2. Duality and the Role of Extreme Points in Linear Approximation

Theory 172

§39.3. Interpolation Property of Subspaces and Uniqueness 175

§39.4. Ascent Method and the Abstract Alternation Theorem 177

§39.5. AppUcation to Chebyshev Approximation 180

EXTREMAL PROBLEMS WITHOUT SIDE CONDITIONS

CHAPTER 40

Free Local Extrema of Differentiable Functionals and the Calculus

of Variations 189

§40.1. nth Variations, G-Derivative, and F-Derivative 191

§40.2. Necessary and Sufficient Conditions for Free Local Extrema 193

§40.3. Sufficient Conditions by Means of Comparison Functionals and

Abstract Field Theory 195

§40.4. AppUcation to Real Functions in RN 195

§40.5. AppUcation to Classical Multidimensional Variational Problems

in Spaces of Continuously Differentiable Functions 196

§40.6. Accessory Quadratic Variational Problems and Sufficient

Eigenvalue Criteria for Local Extrema 200

§40.7. AppUcation to Necessary and Sufficient Conditions for Local

Extrema for Classical One-Dimensional Variational Problems 203

CHAPTER 41

Potential Operators 229

§41.1. Minimal Sequences 232

§41.2. Solution of Operator Equations by Solving Extremal Problems 233

§41.3. Criteria for Potential Operators 234

§41.4. Criteria for the Weak Sequential Lower Semicontinuity of

Functionals 235

§41.5. AppUcation to Abstract Hammerstein Equations with Symmetric

Kernel Operators 237

§41,6. AppUcation to Hammerstein Integral Equations 239

CHAPTER 42

Free Minima for Convex Functionals, Ritz Method and the

Gradient Method 244

§42.1. Convex Functionals and Convex Sets 245

§42.2. Real Convex Functions 246

Contents

§42.3. Convexity of F, Monotonicity of F', and the Definiteness of the

Second Variation 247

§42.4. Monotone Potential Operators 249

§42.5. Free Convex Minimum Problems and the Ritz Method 250

§42.6. Free Convex Minimum Problems and the Gradient Method 252

§42.7. Application to Variational Problems and Quasilinear Elliptic

Differential Equations in Sobolev Spaces 255

EXTREMAL PROBLEMS WITH SMOOTH SIDE CONDITIONS

CHAPTER 43

Lagrange Multipliers and Eigenvalue Problems 273

§43.1. The Abstract Basic Idea of Lagrange Multipliers 274

§43.2. Local Extrema with Side Conditions 276

§43.3. Existence of an Eigenvector Via a Minimum Problem 278

§43.4. Existence of a Bifurcation Point Via a Maximum Problem 279

§43.5. The Galerkin Method for Eigenvalue Problems 281

§43.6. The Generalized Implicit Function Theorem and Manifolds in

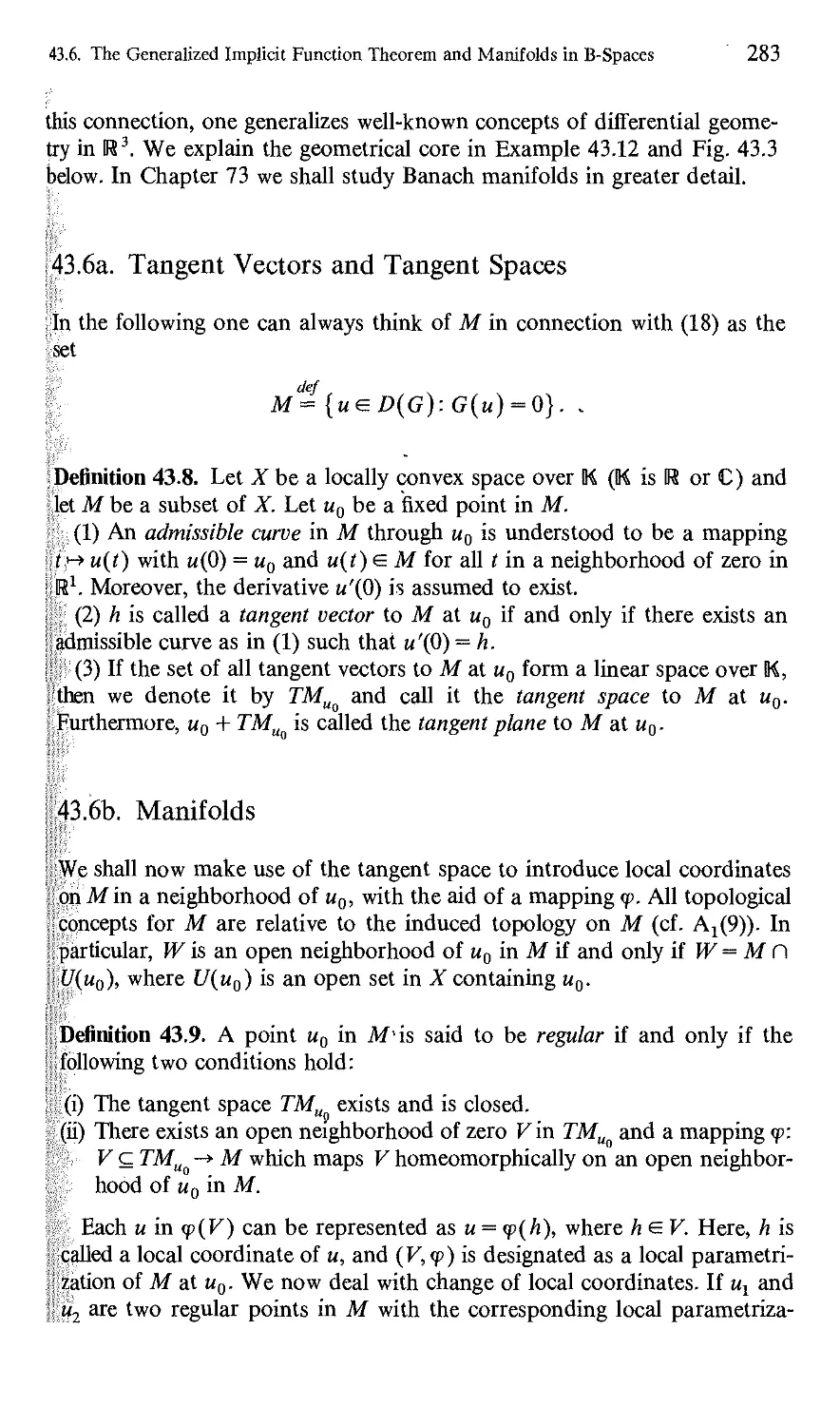

B-Spaces 282

§43.7. Proof of Theorem 43.C 288

§43.8. Lagrange Multipliers 289

§43.9. Critical Points and Lagrange Multipliers 291

§43.10. Application to Real Functions in R N 293

§43.11. Application to Information Theory 294

§43.12, Application to Statistical Physics. Temperature as a Lagrange

Multiplier 296

§43.13. Application to Variational Problems with Integral Side Conditions 299

§43.14. Application to Variational Problems with Differential Equations

as Side Conditions 300

CHAPTER 44

Ljusternik-Schnirelman Theory and the Existence of

Several Eigenvectors 313

§44.1. The Courant Maximum-Minimum Principle 314

§44.2. The Weak and the Strong Ljusternik Maximum-Minimum

Principle for the Construction of Critical Points 316

§44.3. The Genus of Symmetric Sets 319

§44.4. The Palais-Smale Condition 321

§44.5. The Main Theorem for Eigenvalue Problems in Infinite-

Dimensional B-spaces 324

§44.6. A Typical Example 328

§44.7. Proof of the Main Theorem 330

^UlllCllLS

§44.8. The Main Theorem for Eigenvalue Problems in Finite-

Dimensional B-Spaces 335

§44.9. Application to Eigenvalue Problems for Quasilinear Elliptic

Differential Equations 336

§44.10. Application to Eigenvalue Problems for Abstract Hammerstein

Equations with Symmetric Kernel Operators 337

§44.11. Application to Hammerstein Integral Equations 339

§44.12. The Mountain Pass Theorem 339

CHAPTER 45

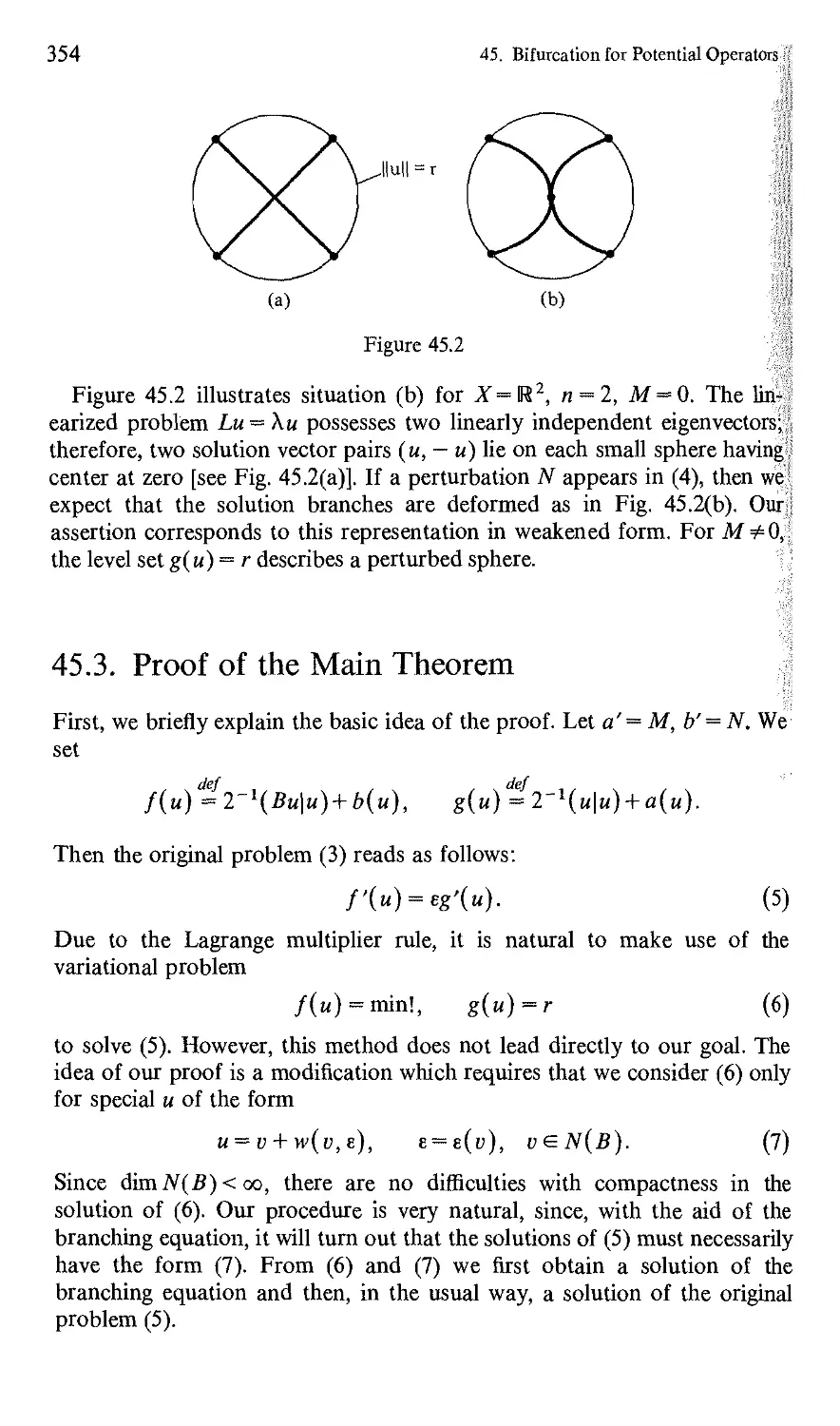

Bifurcation for Potential Operators - 351

§45.1. Krasnoselskii's Theorem 351

§45.2. The Main Theorem • 352

§45.3. Proof of the Main Theorem 354

EXTREMAL PROBLEMS WITH GENERAL SIDE CONDITIONS

CHAPTER 46

Differentiable Functionals on Convex Sets 363

§46.1. Variational Inequalities as Necessary and Sufficient Extremal

Conditions 363

§46.2. Quadratic Variational Problems on Convex Sets and Variational

Inequalities 364

§46.3. Application to Partial Differential Inequalities 365

§46.4. Projections on Convex Sets 366

§46.5. The Ritz Method 367,

§46.6. The Projected Gradient Method 368

§46.7. The Penalty Functional Method 370

§46.8. Regularization of Linear Problems 372

§46.9. Regularization of Nonlinear Problems 375

CHAPTER 47

Convex Functionals on Convex Sets and Convex Analysis 379

§47.1. The Epigraph 380

§47.2. Continuity of Convex Functionals 383

§47.3. Subgradient and Subdifferential 385

§47.4. Subgradient and the Extremal Principle 386

§47.5. Subgradient and the G-Derivative 387

§47.6. Existence Theorem for Subgradients 387

§47.7. The Sum Rule 388

XX

Contents

§47.8. The Main Theorem of Convex Optimization 390

§47.9. The Main Theorem of Convex Approximation Theory 392

§47.10. Generalized Kuhn-Tucker Theory 392

§47.11. Maximal Monotonicity, Cyclic Monotonicity, and Subgradients 396

§47.12. Application to the Duality Mapping 399

CHAPTER 48

General Lagrange Multipliers (Dubovickii-Miljutin Theory) 407

§48.1. Cone and Dual Cone 408

§48.2. The Dubovickii-Miljutin Lemma 411

§48.3. The Main Theorem on Necessary and Sufficient Extremal

Conditions for General Side Conditions 413

§48.4. Application to Minimum Problems with Side Conditions in the

Form of Equalities and Inequalities 416

§48.5. Proof of Theorem 48.B 419

§48.6. Application to Control Problems (Pontrjagin's Maximum

Principle) 422

§48.7. Proof of the Pontrjagin Maximum Principle 426

§48.8. The Maximum Principle and Classical Calculus of Variations 433

§48.9. Modifications of the Maximum Principle 435

§48.10. Return of a Spaceship to Earth 437

SADDLE POINTS AND DUALITY

CHAPTER 49

General Duality Principle by Means of Lagrange Functions

and Their Saddle Points 457

§49.1. Existence of Saddle Points 457

§49.2. Main Theorem of Duality Theory 460

§49.3. Application to Linear Optimization Problems in B-Spaces 463

CHAPTER 50

Duality and the Generalized Kuhn-Tucker Theory 479

§50.1. Side Conditions in Operator Form 479

§50.2. Side Conditions in the Form of Inequalities 482

CHAPTER 51

Duality, Conjugate Functionals, Monotone Operators and Elliptic

Differential Equations 487

§51.1. Conjugate Functionals 489

§51.2. Functionals Conjugate to Differentiable Convex Functionals 492

XXI

§51.3. Properties of Conjugate Functional 493

§51.4. Conjugate Functionals and the Lagrange Function 496

§51.5. Monotone Potential Operators and Duality 499

§51.6. Applications to Linear Elliptic Differential Equations, Trefftz's

Duality 502

§51.7. Application to Quasilinear Elliptic Differential Equations 506

CHAPTER 52

General Duality Principle by Means of Perturbed Problems and

Conjugate Functionals 512

§52.1. The S-Functional, Stability, and Duality . 513

§52.2. Proof of Theorem 52.A 515

§52.3. Duality Propositions of Fenchel-Rockafellar Type 517

§52.4. Application to Linear Optimization Problems in Locally Convex

Spaces 519

§52.5. The Bellman Differential Inequality and Duality for Nonconvex

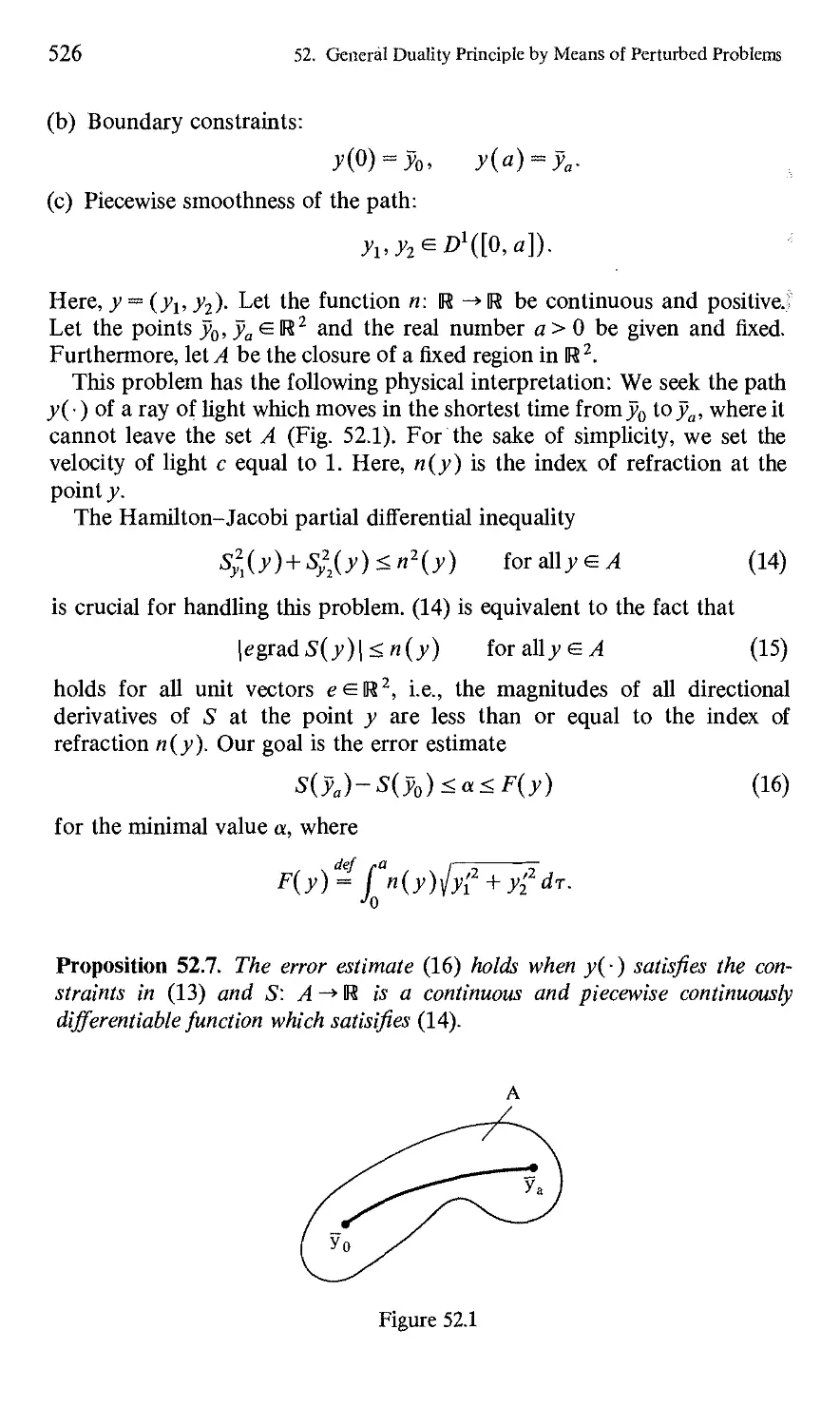

Control Problems 521

§52.6. Application to a Generalized Problem of Geometrical Optics 525

CHAPTER 53

Conjugate Functionals and Orlicz Spaces 538

§53.1. Young Functions 538

§53.2. Orlicz Spaces and Their Properties 539

§53.3. Linear Integral Operators in Orlicz Spaces 541

§53.4. The Nemyckii Operator in Orlicz Spaces 542

§53.5. Application to Hammerstein Integral Equations with Strong

Nonlinearities 542

§53.6. Sobolev-Orlicz Spaces 544

VARIATIONAL INEQUALITIES

CHAPTER 54

Elliptic Variational Inequalities 551

§54.1. The Main Theorem 551

§54.2. Application to Coercive Quadratic Variational Inequalities 552

§54.3. Semicoercive Variational Inequalities 553

§54.4. Variational Inequalities and Control Problems 556

§54.5. Application to Bilinear Forms 558

§54.6. Application to Control Problems with Elliptic Differential

Equations 559

§54.7. Semigroups and Control of Evolution Equations 560

lints

§54.8. Application to the Synthesis Problem for Linear Regulators 561

§54.9. Application to Control Problems with Parabolic Differential

Equations 562

CHAPTER 55

Evolution Variational Inequalities of First Order in H-Spaces 568

§55.1. The Resolvent of Maximal Monotone Operators 569

§55.2. The Nonlinear Yosida Approximation 570

§55.3. The Main Theorem for Inhomogeneous Problems 570

§55.4. Application to Quadratic Evolution Variational Inequalities of

First Order 572

CHAPTER 56

Evolution Variational Inequalities of Second Order in H-Spaces 577

§56.1. The Main Theorem 577

§56.2. Application to Quadratic Evolution Variational Inequalities of

Second Order 578

CHAPTER 57

Accretive Operators and Multivalued First-Order Evolution

Equations in B-Spaces 581

§57.1. Generalized Inner Products on B-Spaces 582

§57.2, Accretive Operators 583

§57.3, The Main Theorem for Inhomogeneous Problems with

m-Accretive Operators 584

§57.4. Proof of the Main Theorem 585

§57,5. Application to Nonexpansive Semigroups in B-Spaces 593

§57.6. Application to Partial Differential Equations 594

Appendix 599

References 606

List of Symbols 637

List of Theorems 643

List of the Most Important Definitions 647

Index 651

Introduction to the Subject

I love mathematics not only because it is applicable to technology but also

because it is beautiful.

Rosza Peter

Science is a first class piece of furniture for the bel etage—as long as common

sense reigns on the ground floor.

Oliver Wendell Holmes

Extremal problems play an extraordinarily large role in the application of

mathematics to practical problems, for example:

(a) in mathematical physics (mechanics and celestial mechanics,

geometrical optics, elasticity theory, hydrodynamics, rheology, relativity theory,

etc.);

(0) in geometry (geodesies, minimal surfaces, etc.);

(•y) in mathematical economics (transport problems, optimal warehouse

maintenance);

(§) in regulation technology (optimal control of general regulation systems,

e.g., industrial installations, spaceships, etc.);

(e) in chemistry, geophysics, technology, etc. (optimal determination of

unknown data from measurements);

(f) in numerical mathematics (optimal structuring of approximation

processes, etc.);

(rj) in the theory of probability (optimal control of stochastic processes,

optimal estimation of unknown parameters, optimal construction of

airplanes, water-power networks, etc.).

2

Introduction to the Subject

In this connection, we exploit the fact that many processes in nature

proceed according to extremal principles, for example:

(a) the principle of stationary action in mechanics, relativity theory,

electrodynamics, etc.;

(b) the principle of minimal potential energy in stable mechanical

equilibrium states;

(c) Fermat's principle of least time in light propagation in geometrical

optics;

(d) Einstein's principle of the motion of mass along four-dimensional

geodesies in general relativity theory.

Moreover, for economic reasons, we are interested in the optimal modelling

of production procedures and other regulation processes.

The history of extremal problems comprises four distinct stages:

(i) The solution of extremal problems for real functions with the aid of

the differential and integral calculus that was invented about 300 years ago.

(ii) Classical calculus of variations that originated about 300 years ago in

connection with mechanical problems.

(iii) Optimization that came into being because of economic and

regulation-technical questions and that has been intensively advanced during

approximately the last 30 years (linear optimization, Kuhn-Tucker theory,

Bellman dynamic optimization, Pontrjagin's maximum principle).

(iv) The theory of variational inequalities and quasivariational inequalities

with its applications to mathematical physics and the deterministic and

stochastic optimization theory that has existed for about the last 15 years.

Figure 37.1 gives a general view. In this connection, we generally

distinguish:

(a) Problems without side conditions (free problems).

(b) Problems with side conditions (bound problems).

Side conditions in the form of equations are typical for the classical calculus

of variations. For example, the shortest path joining two points on a sphere

must satisfy the equation of the sphere. On the other hand, side conditions

in the form of inequalities are typical for optimization. For example, it can

be a matter of bounds for the fuel supply under optimal control of a rocket

or the bounds for the warehouse capacity under optimal warehouse

maintenance.

In the comprehensive introductory chapter (Chapter 37), we give as an

explanation of Fig. 37.1 a survey of diverse concrete formulations of

problems, the calculus of variations, and optimization theory. In the

following chapters we show that these seemingly very disparate problems can be

treated in a unified way within the framework of a functional analytical

theory with the aid of only a few general fundamental principles.

In the following we shall go into several of these interrelationships.

NONLINEAR FUNCTIONAL ANALYSIS

stochastic optimization

EXTREMAL PROBLEMS

VARIATIONAL PROBLEMS,

Euler

differential

equations

(e.g., boundary

and boundary

eigenvalue

problems for

quasilinear elliptic

differential equations)

Variatiomal inequalities

(e.g., differential

inequalities)

..OPTIMIZATION^

/ ..game theory

Hammerstein

integral

equations

discrete

(dynamic optimization

and the discrete maximum

principle)

parameter identification

continuous

(Pontrjagin maximum

principle and the

Bellman equation)

\ I

approximation theory

I

' CONVEX OPTIMIZATION

(Kuhn-Tucker theory)

linear

optimization

Figure 37.1, Overview of extremal problems.

4

Introduction to the Subject

General Basic Ideas

By extremal problems we mean:

(i) minimum and maximum problems (extremal problems in the narrower

sense);

(ii) saddle point problems and minimax problems (game theory, duality

theory and error estimates, approximation theory);

(iii) determination of critical points (eigenvalue problems, Ljuster-

nik-Schnirelman theory, and Morse theory);

(iv) determination of noncooperative equilibrium points in the sense of

Nash, Pareto optimization, Walras equilibria (economics models);

(v) solution of variational inequalities.

Here, (iv) [respectively, (v)] is related to (ii) [respectively, (i)]. The concept of

critical point is of central significance for variational problems and their

applications. The functional F has a critical point with respect to a

neighborhood U of «0 in case, roughly speaking, the following holds: The

differenceF(u0 + h)— F(u0) is of order greater than the first with respect to

all h such that uQ + heU. For a real function F: R ->R this means that

F'(uQ) = 0 provided 1/= R. The precise definition of a critical point can be

found in Section 43.9. The intuitive meaning of a critical point is explained

in Sections 37.1. and 37.2 for real functions of one and several variables as

well as for free variational problems (respectively, variational problems with

side conditions) in 37.4b (respectively, 37.4/). In Section 43.9 we go into the

connection between critical points and Lagrange multipliers. If F has a

critical point at u0, then we also say that Fis stationary at u0. We symbolize

the problem of discovering critical points u of F with respect to U by

F(u) = stationary!, «e[/.

Many equations of mathematical physics are obtained from such

formulations of the problem (principle of stationary action). Moreover, the

symmetry properties of F lead, via the Noether theorem (cf. 37.4k), to physical

conservation quantities (energy, spin, etc.) and transformation properties of

the field equations (tensors, spinors, and gauge transformations). This is

u

Figure 37.2

General Basic Ideas

5

especially important if one wishes, for example, to obtain an overview of the

possible field equations on the basis of physical symmetry and invariance

ideas for interacting quantum fields of elementary particles.

To fix the terminology, we now recall several well-known concepts. We

designate minima and maxima as extrema. A general minimum problem has

the form

infF(«) = a. (l°)

ae(/

Here, F: U-* [ — 00,00] is a mapping that can take on the two values ± 00

besides all real values. In the introduction to Chapter 47 we explain why

taking these two improper values into consideration is very expedient.

Posing the problem in the form (1°) means that the infimum a of F is

sought on U. This infimum always exists on [—00,00]. By definition, it is

equal to the greatest lower bouqid of the values of F on U. The point uQ in U

is called a solution of (1°) or, also, a minimal point of F on U if and only if

F(u0) = a. In this case, we call a the minimal value of F on U. Moreover,

we say that F possesses a minimum on U.

If we wish to emphasize that we are seeking a minimal point, then instead

of (1°) we write

minF(«) = a. (2°)

ae(/

This way of formulating the problem thus entails the determination of the

infimum a of F on U and discovering a u0 in U such that F(u0) = a. Figure

37.2 refers to the important situation that a solution u0 of (1°) [respectively,

(2°)] need not always exist. For (1°) [respectively, (2°)] we occasionally

write

F( u) = inf., «e[/; respectively F( u) = min!, u e U.

Maximum problems of the form

sup F(u) = /3, (3°)

ae(/

maxF(tt)=)8 (4°)

ae(/

are to be understood analogously. By definition, we set the infimum

(respectively, the supremum) over the empty set U = 0 in (1°) [respectively, (3°)]

equal to a = + 00 (respectively, /3 = — 00). We shall frequently be concerned

with minimum problems only, since, because of the relation

supF(«) = - inf (-F(u)), (5°)

ae(7 ae(7

every maximum problem can be changed into a minimum problem by

switching from F to — F.

We designate problems of the type

mini sup L(x, y)) = y (6°)

6

Introduction to the Subject

as min-sup problems. The point x is a solution of (6°) if and only if, parallel

to our conventions for (1°) and (2°), we have

def / ,\

y = inf I sup L(x, y)\

x^A^y&B '

and

sup (L(x, .)0) = 7, x^A. (6a°)

yeB

If we replace the symbol "sup" by "max" in (6°), then (3c, y) is naturally

called a solution of (6°) if and only if y is a solution of (6a°). max-inf

problems, etc., are handled analogously. It is thus clear what is to be

understood by a solution (x, y) of

min sup L(x,y) = max inf L(x, y), (7°)

i€A ye B yeBxe A

namely,

del

y = inf sup L(x,y)= sup infL(x,>')

je/l jet y^BxeA

and

supL(x,>') = v, inf L(x,y) = y, (x,y)^AxB. (7a°)

One is led to (7°) when determining the saddle points (x, y) for L. If the

symbols "max" and "min" appear instead of "sup" and "inf in (7°), then

(x, y) is called a solution of the corresponding minimax problem if and only

if (7a°) holds for y = L(x,y). Problems of the form (6°) appear, for

example, in approximation theory, for one can write the problem

min||fc-x|| = -y

x e A

as

min max (y, b - x) = y,

where A C X and B= {y e X*: \\y\\ =1} in case X is a B-space. (7°) and the

corresponding minimax problems are basic to the game theory discussed in

Section 37.8 and to the duality theory in Chapter 49.

In Part III, we shall investigate the following central questions for

extremal problems:

(a) Existence and uniqueness of extremal solutions (minimal and maximal

points, saddle points, equilibrium points, critical points).

(b) Necessary and sufficient conditions for characterizing extremal

solutions.

(c) Construction of approximation methods for calculating the extremal

values a, /3, y and the extremal solutions, obtaining error estimates.

(d) Connections between various extremal problems by means of duality

theory.

(e) Estimates for the number of critical points (Morse theory and

General Basic Ideas

7

In this connection, let us elucidate several fundamental notions. In Parts I

and II we placed the fixed point theorems of Banach, Schauder, and

Bourbaki-Kneser at the pinnacle of nonlinear functional analysis. The

existence propositions for extremal solutions are based on:

(a) Compactness (generalized Weierstrass theorem).

(/?) Convexity (separation of convex sets, Hahn-Banach theorem).

We carry this out more precisely in Chapters 38 and 39. The compactness

arguments in Chapter 38 generalize the classical Weierstrass theorem: A

continuous real function on a closed bounded interval has a minimum and a

maximum. Existence propositions that are based on convexity arguments as

in Chapter 39 are frequently intimately connected with duality theory. In

this connection, together with a given minimum problem, we consider a

corresponding maximum problem. The prototype for this is shown in Fig.

37.3. The original problem reads as follows:

min||fc-w|| = a, (8a°)

u e<7

i.e., we seek the minimal Euclidean distance of the point b in R3 from the

straight line U- The corresponding dual problem reads as follows:

maxdist(b,H) = P, (8b°)

i.e., we seek the maximal Euclidean distance of the point b from all planes

H that pass through the straight line U. In the present case, a = /3. For

extremal problems in infinite-dimensional spaces, it is frequently the case

that for two given mutually dual problems one can obtain existence

propositions for one of the problems by a compactness argument and for the other

by a convexity argument. However, it is also possible that the given problem

has no solution, but that the dual problem does. This makes the

construction of generalized solutions for the original problem possible. One exploits

this situation, for instance, in the theory of minimal surfaces (Chapter 52).

Uniqueness propositions for the minimum problem

infF(«) = a (9°)

are based in general on one of the following two principles:

(a) Condition on F (strict convexity).

(/?) Condition on U (interpolation property).

bT H

0

Introduction to the Subject

/

(a)

Figure 37.4

(b)

In Fig. 37.4(a), F is strictly convex and has, in contrast to Fig. 37.4(b), a

uniquely determined minimal point. In order to elucidate the prototype for

conditions on U, we consider (9°), with u = ((,if), \\u\\ = max(|£|, M), F =

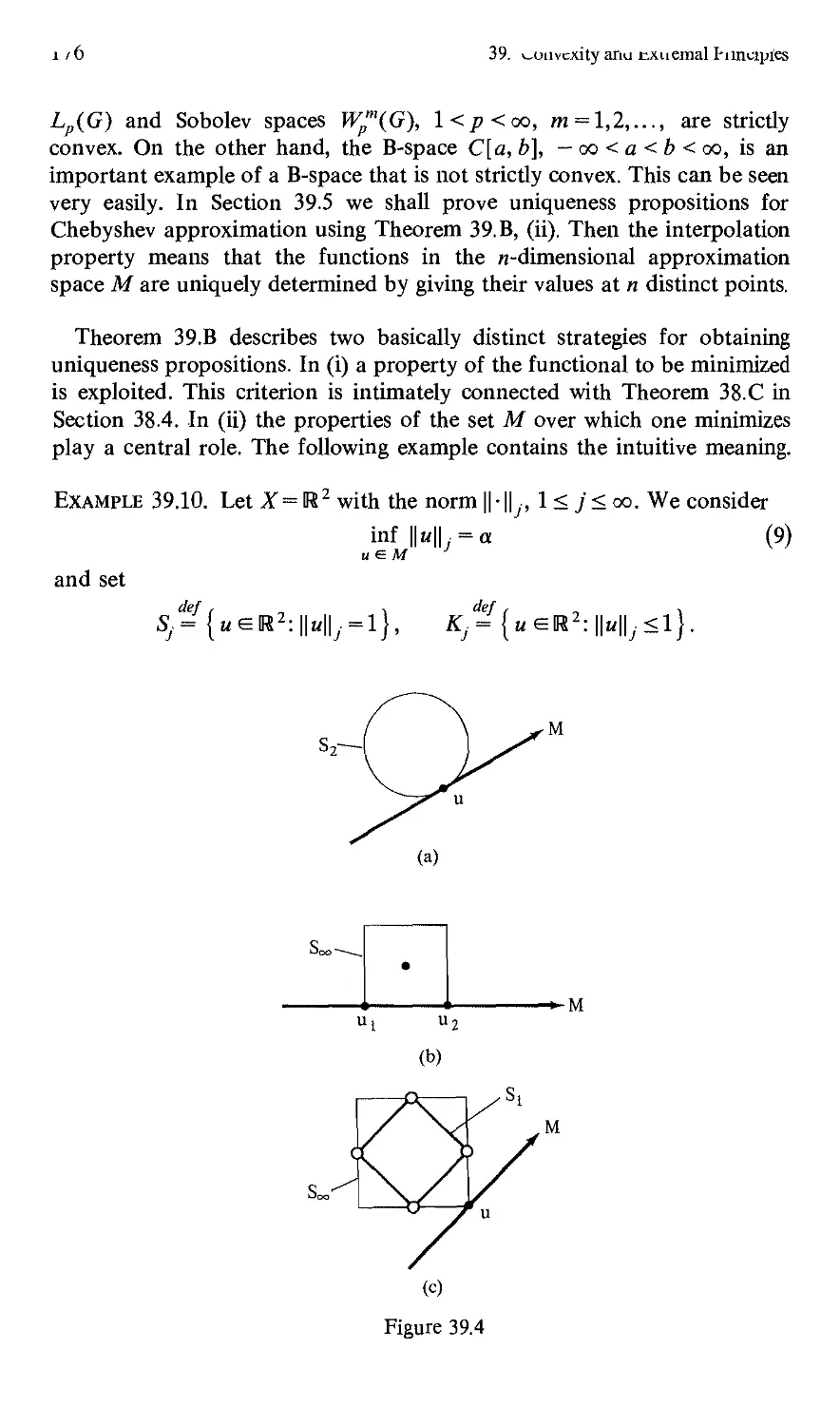

\\u\\. Let U be a straight line. The set Q = {«eR2: ||h||=1} is the boundary

of the unit square. In Fig. 37.5(a), (9°) has exactly one solution, whereas in

Fig. 37.5(b) there exist infinitely many solutions. The solutions are exactly

all the points of dQ that lie on U. Moreover, a ==1. In Section 39.2 we

explain the connection with the so-called interpolation property of U. In

classical Chebyshev interpolation, the interpolation property is known as

the Haar condition.

The necessary conditions for solutions u of the minimum problem (9°)

can, to begin with, be split, roughly speaking, into two classes:

(a) the operator equation F'(u) = 0 (free minimum, u is an interior point of

U);

(fi) the Lagrange multiplier rule (minimum with side conditions).

Furthermore, there are, in addition:

(y) sub gradient condition 0 e dF(u);

(S) variational inequalities;

(e) characterization of solutions by means of dual problems.

In Parts I and II we were greatly concerned with the solution of operator

equations which one can always write in the form

Bu = 0. (10°)

The connection with extremal problems is roughly the following: If F has a

derivative F', then for an interior point u0 of U we have: If uQ is a solution

of (9°), then F'(«(,) = °-

(a)

Figure 37.5

(b)

ijeneral Basic Ideas

9

It follows from this that there is an important method for the solution of

the operator equation (10°) which, for example, can represent a differential

equation, an integral equation, or a system of real equations: We seek a

functional F such that B = F' and solve the minimum problem (9°) or a

corresponding maximum problem. However, it suffices that u0 be a critical

point—for instance, a saddle point. Then we also have F'(«0) = 0. In any

case, it must be emphasized that not all operators B can be written in the

form B = F' but rather only the so-called potential operators. In a real

Hilbert space, of the continuous linear operators it is precisely and solely

the self-adjoint operators that are also potential operators. We give general

criteria for an operator to be a potential operator in Section 41.3.

Especially strong propositions can be proved for the minimum problem

(9°) in case where Fis convex. F' is then a monotone operator. We studied

the theory of monotone operators in Part II. Not every monotone operator

is a potential operator. However, for monotone potential operators, one can

prove additional propositions— for instance, propositions for eigenvalue

and bifurcation problems. We discuss this in Chapters 43-45.

During the last 15 years, in connection with optimization problems, a

convex analysis for convex, but not necessarily differentiable, functionals

has been formulated. At the center of this theory there stands a calculus for

the subdifferential dF(u) which appears in place of the derivative F'(u).

The basic idea, which leads to the definition of dF(u), is elucidated in

Section 37.2. The necessary condition F'(«) = 0 is then replaced by 0 e

dF(u). Chapters 47 and 51-53 are devoted to convex analysis. There we

also work out the interrelationship between conjugate functionals and

duality theory.

If the minimum problem (9°) has a solution u0 which is not an interior

point of U, then more complicated necessary conditions appear for u0,

which in many cases can be summarized in a unified way under the concept

of the Lagrange multiplier rule. In general, one is led to Lagrange

multipliers if the side conditions occur in the form of equations or inequalities.

Prototypes for this are:

(a) Eigenvalue problems.

(/?) Linear or convex optimization problems.

We elucidate these prototypes in Sections 37.3, 37.6, 37.10, and 37.11.

Moreover, in Section 37.10 we also obtain the connection between the

Lagrange multiplier method and duality theory. We delve more deeply into

this interrelationship in Chapter 50. Furthermore, in Chapter 43

(respectively, Chapter 48) we justify the Lagrange multiplier method for smooth

(respectively, more general) side conditions. At this point we already note

the important situation that the Lagrange multiplier rule in the narrower

sense is tied up with certain nondegeneracy conditions. The purely formal

application of the Lagrange multiplier rule which one frequently finds in

physics textbooks can lead to false results. One finds a counterexample to

this in Section 43.1.

10

Introduction to the Subject

If U in (9°) is convex and F' exists, then the variational inequality

(F'{u0),v-u0)>0 for all ue U (11°)

holds for a solution uQ of (9°). In Section 37.1 we explain that this is a

matter of the generalization of a well-known necessary condition for the

existence of minima of real functions. A quasivariational inequality is

present when, in addition, U in (11°) depends on u0. Instead of (11°) we

shall consider more general problems, e.g.,

(Au0— b,v — u0) >h(v)— h(u0) for all v e U,

where the operator A is not necessarily a potential operator. The theory of

variational inequalities that has been developed over the last 15 years

combines the theory of extremal problems and the theory of monotone

operators under a unified viewpoint. In Chapter 9 we explained the

important connections with the theory of multivalued mappings. We concern

ourselves with variational inequalities in Chapters 46 and 54-57.

The sufficient conditions for the existence of solutions of the minimum

problem (9°) can be roughly classified as follows:

(a) Positive definiteness of the second variation.

(/?) Characterization of solutions by means of the dual problem.

(•y) Comparison functionals (abstract field theory).

(5) The method of dynamic optimization.

(e) In case of convex problems, the necessary conditions are generally

sufficient.

The criteria that use the second variation are discussed in Section 40.2 (free

local minima) and in Section 43.8 (Lagrange multiplier rule). In this

connection, this is a matter of a generalization of the known classical

criterion for real functions: F"(u0)>0 implies the existence of a local

minimum for F at u0 in the case F'(uQ) = 0. We point out the advantages of

dual problems for the characterization of solutions in Section 37.29f. In

Section 37.20b (respectively, Section 40.3), we treat the method of dynamic

optimization (respectively, the method of comparison functionals). In

Section 40.7 we elucidate the connection between the abstract results and the

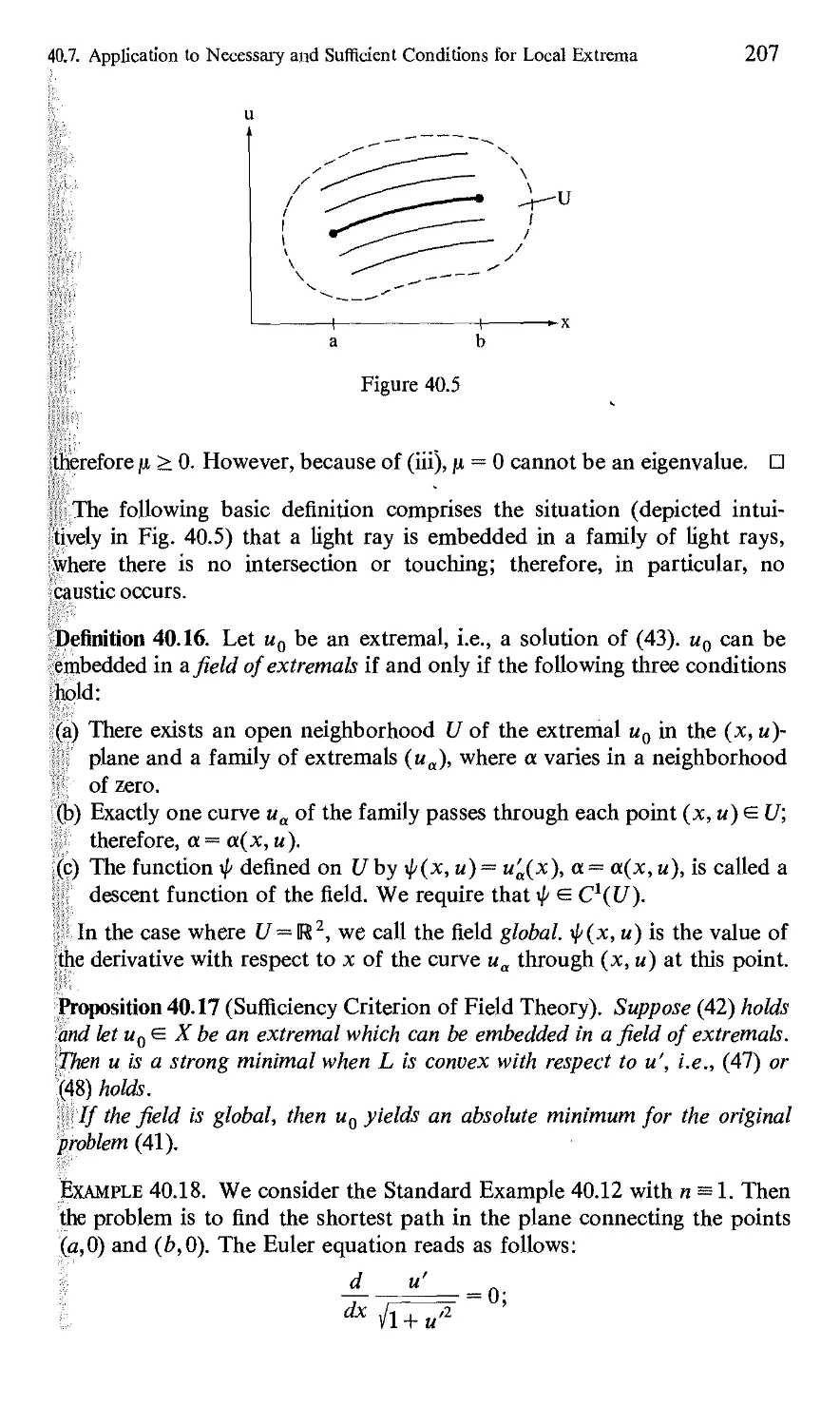

field theory of classical calculus of variations.

In order to make it easier for the reader to learn the essential ideas in the

construction of approximation methods for extremal problems, we present,

in Section 37.29, the basic ideas of various important approximation

methods:

(i) The Ritz method (projection method),

(ii) The gradient method (descent method),

(iii) Ascent method,

(iv) Penalty method.

(v) Regularization.

(vi) Duality method.

General Basic Ideas

11

(vii) Dynamic optimization,

(viii) Decomposition,

(ix) Equivalence and combination principle.

These basic ideas are delved into more deeply later.

In conclusion, we summarize the advantages of duality theory:

(a) Necessary and sufficient conditions for the characterization of extremal

solutions.

(b) Existence propositions when properties of the corresponding dual

problems that are frequently easy to verify are at hand.

(c) The construction of generalized solutions for unsolvable problems with

the aid of solutions of the dual problem and the so-called extremal

relation.

(d) The construction of approximation methods with two-sided error

estimates for the extremal values and error estimates for the extremal

solutions.

(e) The side conditions of the dual problem may have a simpler structure

than that of the original problem; therefore, it is occasionally more

propitious to solve the dual problem and to obtain solutions for the

original problem by means of the extremal relation.

We explain this in Section 37.29f.

The basic ideas of duality theory can be found in Chapter 39.

Furthermore, we take up duality theory in detail in Chapters 49-53.

In Part I, the topological essence of fixed point theory concentrated on

the concept of the fixed point index (mapping degree). In the theory of

extremal problems, topological tools will be used to obtain, within the

framework of the Morse theory and the Ljusternik-Sclinirelman theory,

estimates for the smallest number of critical points and to guarantee the

existence of at least one saddle point in indefinite problems. From this we

obtain, for example, propositions concerning the number of eigensolutions

for nonlinear differential and integral equations or concerning the number

of geodesies (Chapter 44) as well as concerning the existence of solutions of

nonlinear differential equations or the existence of periodic solutions of

dynamical systems (Chapter 49).

In the preceding overview it is already apparent that the solutions

of convex minimum problems have especially propitious properties. A goal

of current research consists in making the propitious behavior of convex

problems useful also for classes of nonconvex problems by introducing

generalized concepts of a solution. We discuss this in Chapters 42 and 48.

Finally, we would like to point out that in general we follow the strategy

of reducing propositions on extremal problems for functional to that for

classical real functions. This becomes especially clear in the introduction to

Chapter 40.

CHAPTER 37

Introductory Typical Examples

When I was a student it was fashionable to give courses called "Elementary

Mathematics from the Higher Point of View" But what I needed was a

few courses called " Higher Mathematics from the Elementary Point of View."

Joel Franklin

In the occupation with mathematical problems, a more important role than

generalization is played—I believe—by specialization.

David Hubert

There are two ways to teach mathematics. One is to take real pains toward

creating understanding—visual aids, that sort of thing. The other is the old

British system of teaching until you're blue in the face.

James R. Newman, compiler of the 2,535 page The World of Mathematics,

quoted in the New York Times, Sept. 30,1956

In the following we wish to present many concrete examples, foregoing

extensive technical details, whose solutions have contributed essentially to

the development of a general theory of extremal problems. A glance at the

organization of this chapter in the Contents shows the variety of different

problems one encounters. In this connection, an especially central position

is assumed by Section 37.4, where we discuss a number of fundamental

ideas from the classical calculus of variations. The ideas of the calculus of

variations have influenced the modern theory of extremal problems in an

essential way, and knowledge of these classical ideas is indispensable for a

thorough understanding of the modern development.

In the references to the literature at the end of each section of this

chapter, we restrict ourselves to a few introductory expositions and standard

12

37.1. Real functions in R1

13

works. The later chapters are provided with detailed lists. If the reader

concentrates his attention on the works introduced in the references to the

literature in this chapter under the caption "classical works," then he can

obtain a quick survey of the historical development of the subject.

This chapter addresses itself to readers who are interested in a detailed

motivation of the general theory by means of simple but typical examples.

In the following chapters, we will show how these examples fit into a general

functional analysis theory. In this connection, the reader is often referred to

the corresponding sections of the present chapter. For this reason, a cursory

perusal of this chapter on first reading will suffice. A reader who wishes to

get acquainted immediately with the foundational principles of the theory of

extremal problems can begin with Chapters 38 and 39. There we explain the

role of compactness and convexity for existence propositions, give two

important uniqueness criteria, and treat some fundamental principles of

duality theory.

37.1. Real Functions in Ul

One can already observe numerous phenomena that are typical for extremal

problems in the study of real-valued functions of a real variable. Later we

shall often reduce the investigation of general functionals x>-+ F(x) on a

locally convex space X to the investigation of real-valued functions t >-> <p(t)

of a real variable t, where we set <p(0 = F(x(t)). Here, t >-> x(t) is a curve

inX

Let F: [a, b] -» U be a real function defined on the bounded interval

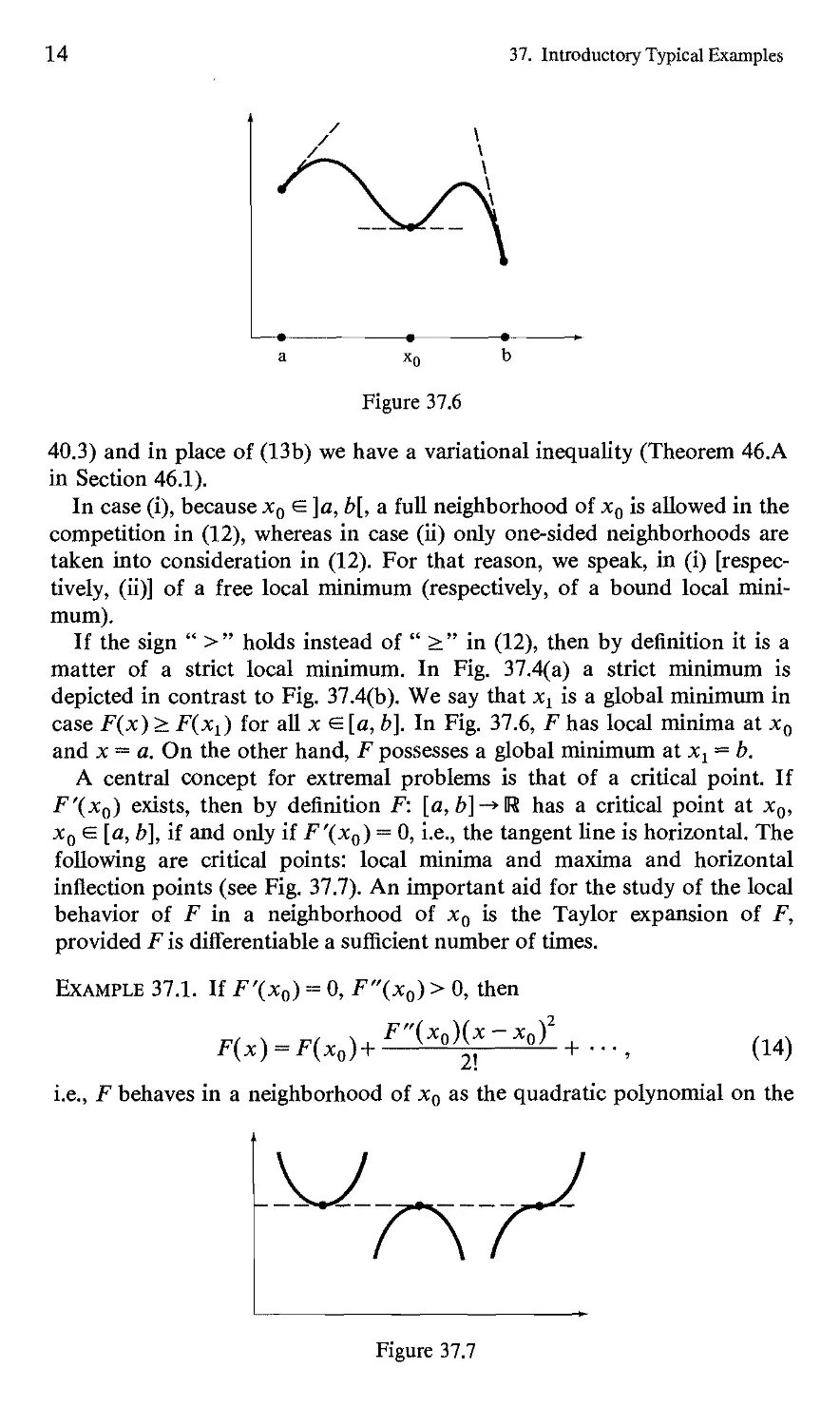

[a, b]. By definition, F has a local minimum at x0 if and only if there exists a

neighborhood U(x0) of x0 such that

F(x)>F(x0) for allx e(/(x0)n[a,fc], where x =£ x0. (12)

If F possesses a local minimum at xQ and the derivative F'(x0) exists, then

one must distinguish two cases:

(i) If x0 is an interior point of [a, b], then

*"(*„)-0. (13a)

(ii) If x0 is a boundary point of [a, b], then

F'(x0)(x-x0)>0 forallxe[a,fc]. (13b)

The condition (13b) is equivalent to F'(x0)>0 [respectively, F'(x0)<0]

for xQ = a (respectively, xQ = b) (see Fig. 37.6). Obviously, (13a) is a special

case of (13b).

If F: D(F) C X-> U is a functional, for instance, on the B-space X, then

in place of (13a) we have an operator equation (Theorem 40.B in Section

37. Introductory Typical Examples

/

/

/

\

\

\

a x0 D

Figure 37.6

40.3) and in place of (13b) we have a variational inequality (Theorem 46.A

in Section 46.1).

In case (i), because x0 e ]a, b[, a full neighborhood of x0 is allowed in the

competition in (12), whereas in case (ii) only one-sided neighborhoods are

taken into consideration in (12). For that reason, we speak, in (i)

[respectively, (ii)] of a free local minimum (respectively, of a bound local

minimum).

If the sign " >" holds instead of " >" in (12), then by definition it is a

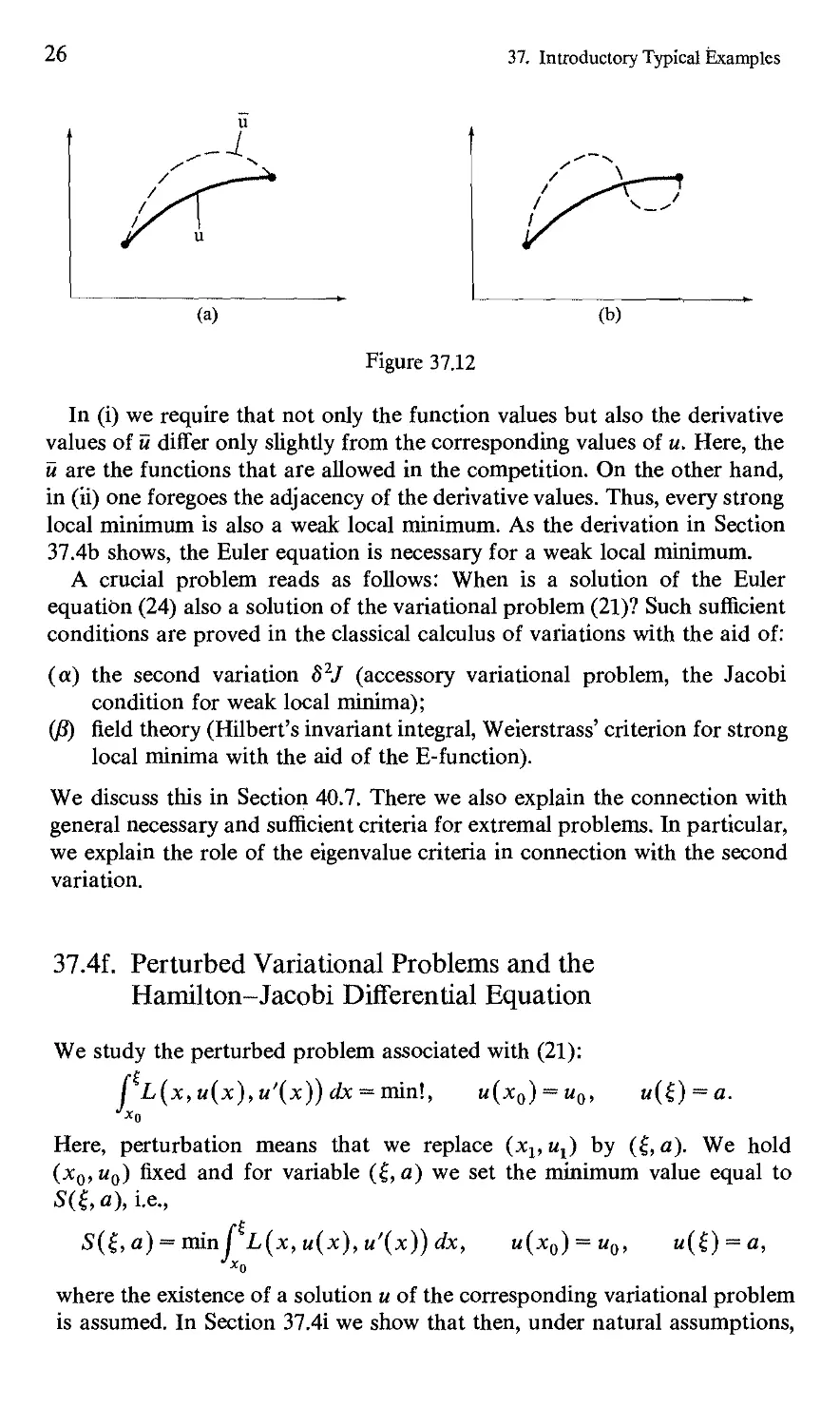

matter of a strict local minimum. In Fig. 37.4(a) a strict minimum is

depicted in contrast to Fig. 37.4(b). We say that xx is a global minimum in

case F(x) > F(xt) for all x e [a, b]. In Fig. 37.6, F has local minima at x0

and x = a. On the other hand, F possesses a global minimum at xx = b.

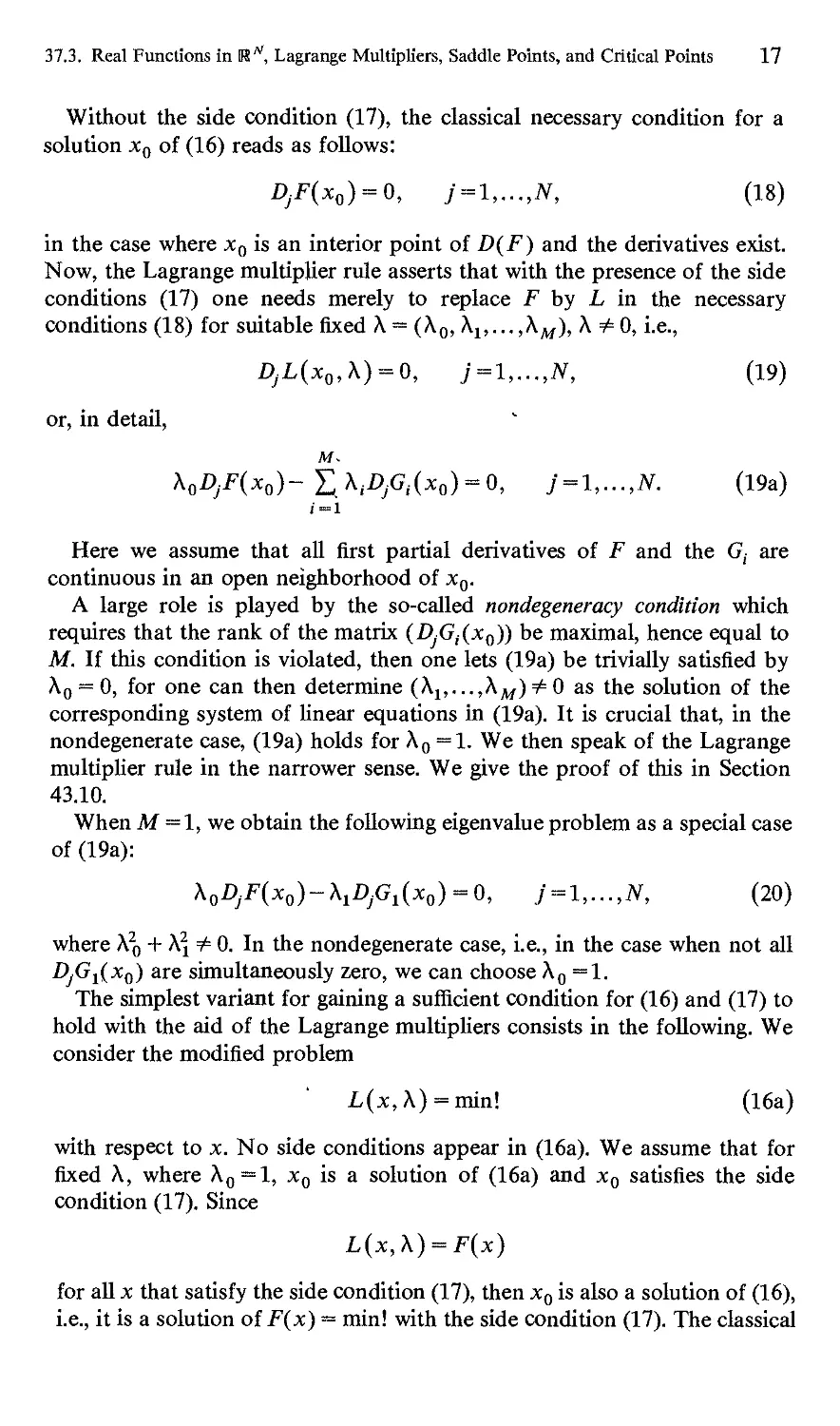

A central concept for extremal problems is that of a critical point. If

F'(x0) exists, then by definition F: [a, b]-*U has a critical point at x0,

x0 e [a, b], if and only if -F'(*o) = 0, i.e., the tangent line is horizontal. The

following are critical points: local minima and maxima and horizontal

inflection points (see Fig. 37.7). An important aid for the study of the local

behavior of F in a neighborhood of x0 is the Taylor expansion of F,

provided F is differentiable a sufficient number of times.

Example 37.1. If F'(x0) = 0, F"(x0) > 0, then

F(x) = F(x0)+F"iXo)^'Xof+---, (14)

i.e., F behaves in a neighborhood of xQ as the quadratic polynomial on the

Figure 37.7

37.2. Convex Functions in R1

15

right-hand side of (14). Consequently, F has a strict local minimum at xQ.

The precise assumptions for this are: F'(x0) = 0, F"(x0)>0, and F" is

continuous at xQ. This follows from the form of the remainder term in (14).

Example 37.2. If F(">(x0) = 0 for « =1, 2, 3, 4 and F(5>(x0) + 0, then

Therefore, x0 is a horizontal inflection point, for F behaves locally as the

fifth-degree polynomial on the right-hand side of the last equation.

The material of this section is contained in any textbook of differential

and integral calculus.

37.2. Convex Functions in U1

A function F: [a, b] -» U is said to be convex if and only if each chord lies

above the corresponding arc of the curve (see Fig. 37.8). In contrast to

arbitrary real functions, convex functions possess a number of remarkable

properties of which we list three here:

(a) If F has a local minimum at x0, then F also has a global minimum at x0.

(b) The necessary conditions (13a) [respectively, (13b)] for local minima are

also sufficient for global minima.

(c) If F' exists on [a, b], then on [a, b\. F is convex if and only if F' is

monotonely increasing.

In Chapter 42, property (c) yields the connection between convex

functional and monotone operators. A convex function possesses only minima as

critical points.

Figure 37.8

16

37. Introductory Typical Examples

Figure 37.9

If F: [a, b] -» U is a convex but not necessarily differentiable function,

then a global minimum at xQ can be characterized by

0 e dF{x0) (15)

instead of by F'(x0) = 0 or (13b). Here, the so-called subdifferential dF(x0)

equals the set of all slopes m of the straight lines through (x0, F(x0)) which

lie beneath the curve determined by F (see Fig. 37.9). (15) is the starting

point for the convex analysis that we develop in Chapter 47.

References to the Literature

Convex analysis and convex sets: Rockafellar (1970, M, H, B) and Roberts,

Varberg (1973, M, B, H) (standard works for RB); Holmes (1972, L), (1975,

M); Ekeland and Temam (1974, M); Marti (1977, M).

37.3. Real Functions in UN, Lagrange Multipliers,

Saddle Points, and Critical Points

We consider the minimum problem:

F(x) = min! (16)

subject to the side conditions

G,.(x) = 0,/=1,...,M, (17)

where x = (^,... ,£N), Dj,= d/d^j. Here, F and all the G,'s are real-valued

functions of the real variables £v...,£N, and M < N.

We denote the corresponding Lagrange function by

M

L(x,A) = A0JF(x)-£A,.G,-(*)-

i-i

All the A,'s are real numbers and are called Lagrange multipliers.

37.3. Real Functions in R^, Lagrange Multipliers, Saddle Points, and Critical Points 17

Without the side condition (17), the classical necessary condition for a

solution xQ of (16) reads as follows:

DjF{x0) = 0, j = l,...,N, (18)

in the case where xQ is an interior point of D(F) and the derivatives exist.

Now, the Lagrange multiplier rule asserts that with the presence of the side

conditions (17) one needs merely to replace F by L in the necessary

conditions (18) for suitable fixed A = (A0, A1;...,AM), A + 0, i.e.,

DjL{x0,X) = 0, j=l,...,N, (19)

or, in detail,

A0Z>yF(x0)-X;A,.Z>,.G,.(x0) = 0, j = l,...,N. (19a)

i=i

Here we assume that all first partial derivatives of F and the G, are

continuous in an open neighborhood of x0.

A large role is played by the so-called nondegeneracy condition which

requires that the rank of the matrix (Z)yG,(x0)) be maximal, hence equal to

M. If this condition is violated, then one lets (19a) be trivially satisfied by

A0 = 0, for one can then determine (A1,...,AM)#0 as the solution of the

corresponding system of linear equations in (19a). It is crucial that, in the

nondegenerate case, (19a) holds for A0 = 1. We then speak of the Lagrange

multiplier rule in the narrower sense. We give the proof of this in Section

43.10.

When M = 1, we obtain the following eigenvalue problem as a special case

of (19a):

A0^(*o)-Ai^Gi(*o)-0, j = l,.-.,N, (20)

where A20 + X\ + 0. In the nondegenerate case, i.e., in the case when not all

DjG^Xq) are simultaneously zero, we can choose A0 =1.

The simplest variant for gaining a sufficient condition for (16) and (17) to

hold with the aid of the Lagrange multipliers consists in the following. We

consider the modified problem

L(x, A) = min! (16a)

with respect to x. No side conditions appear in (16a). We assume that for

fixed A, where A0 = l, x0 is a solution of (16a) and xQ satisfies the side

condition (17). Since

L(x,X) = F(x)

for all x that satisfy the side condition (17), then x0 is also a solution of (16),

i.e., it is a solution of F(x) = min! with the side condition (17). The classical

18

37. Introductory Typical Examples

condition that xQ be a solution of (16a) reads as follows:

(a) (19) holds.

(b) The quadratic form associated with the Hessian matrix (DkDjL(x0, A))

is positive definite.

If all the Gj's are linear, then DkDjL(x0, A) = DkDjF(x0), i.e., A does not

even appear in the Hessian matrix. One must frequently deal with linear

Gj's when studying problems of the type (16) and (17) for determining

thermodynamic equilibrium states (cf. Part IV).

We will make use of this simple method in Section 37.4/ to investigate

variational problems with side conditions. In Section 43.10 we shall prove a

refined sufficiency criterion for (16) and (17).

We now explain the connection with critical points. By definition,

F possesses a critical point at xQ relative to the side condition (17) if and

only if:

(i) If we set f(t) = F(x(t)), then / has a critical point at r = 0, i.e.,

/'(0) = 0.

(ii) Here we shall consider precisely all curves t>-+x(t) which satisfy the

side condition (17) in a neighborhood of t = 0. Moreover, x'(0) must

exist. Furthermore, x(0) = xQ.

In Chapter 43 we shall show that under appropriate regularity

requirements on F and G„ the existence of a critical point for F relative to (17) in

the nondegenerate case is equivalent to (19) and A0 = 1. If no side condition

(17) is at hand, then we talk about a free critical point. If F possesses

continuous first partial derivatives at x0, then we can choose x(t) in (ii) to

have the form x0 + th and obtain from/'(0) = 0, according to the chain rule,

that 2,jDjF(x0)hj = 0 for all h e UN, and thereforeDjF(x0) = 0,/ = 1,...,N;

but this is (18). We can thus characterize a free critical point x0 as follows:

(a) Geometric condition: The tangent plane at x0 is horizontal.

(b) Analytic condition: The linear terms in the Taylor expansion vanish at

the point xQ.

(c) Degeneracy property: The linear approximation F'(*o): R"-» U of F:

U(x0)CUN-*U is not surjective. Observe that F'(x0)h = /)^(½)^

+ ■■■ + DNF(x0)hN holds.

In the theory of manifolds, the definition of a critical point is based on

(c).

Local minima and maxima and saddle points are critical points.

The use of the concept of a saddle point is not uniform in the literature.

By "saddle point" we shall mean any critical point which does not

correspond to a local minimum or a local maximum (cf. Section 43.9). In the

regular case, this means intuitively, in (i) and (ii) above, that there exist two

clef

curves r >-> xx(t) and r >-> x2(t) such that for ft{t) = F{x,{t)): /x has a local

minimum at t = 0, and /2 has a local maximum at t = 0. For example, for

37.3. Real Functions in Rw, Lagrange Multipliers, Saddle Points, and Critical Points 19

the quadratic function F: U2-*U, F(x) = ai-j + b%\, the following

assertions hold:

(a) F possesses a minimum at x = 0 when a, b>0.

(fi) F possesses a maximum at x = 0 when a, b < 0.

(•y) F possesses a saddle point at x = 0 when aft < 0.

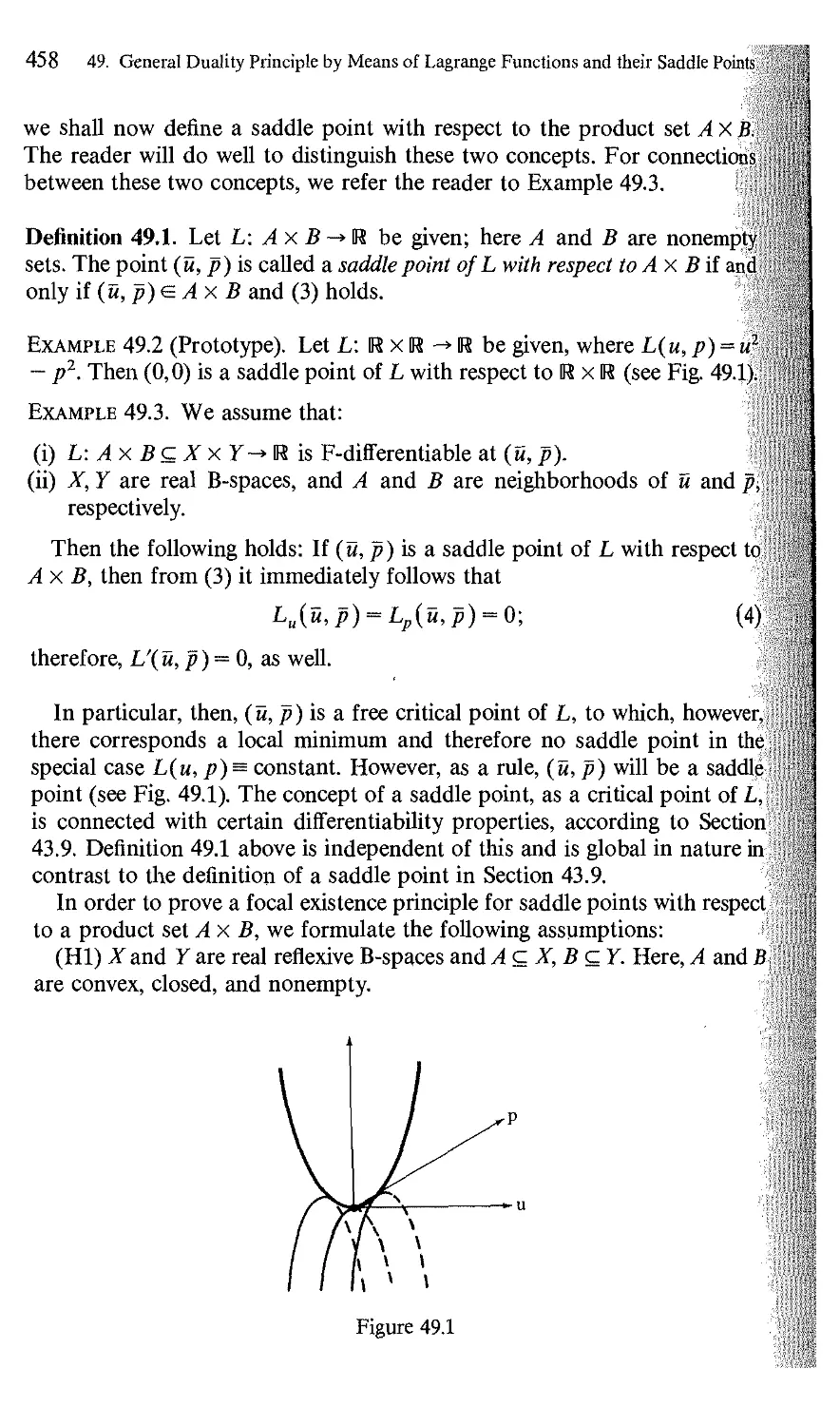

For instance, if a > 0, b < 0, then £\ >-> F(£x, £2) has a minimum at £x = £2 = 0

and £2 >-> F(£1; £2) has a maximum at this point (see Fig. 49.1).

Besides, in connection with duality theory and game theory, we use the

narrower concept of a saddle point with respect to a product set. In this

connection, compare Section 49.1.

In general, one can study the local behavior in a neighborhood of a

critical point parallel to the Examples 37.1 and 37.2 with the aid of the

Taylor expansion. Morse theory provides normal forms for critical points

(cf. Section 37.26).

Saddle points are significant for game theory and duality theory.

Equation (20) shows that one obtains existence propositions for eigenvalue

problems by means of the study of the critical points of functions or, more

generally, of functionals. Existence statements for nonlinear equations of

the type (18) are obtained by constructing free critical points. In Section

44.12 we consider the so-called mountain pass theorem. This theorem

asserts the existence of a nontrivial free critical point.

Estimates for the number of critical points are obtained by using

topological tools within the framework of the Morse theory and the

Ljusternik-Schnirelman theory (cf. Sections 37.26, 37.27, and Chapter 44).

In Section 49.1 we treat a general existence theorem for saddle points with

respect to product sets. In the Problems for Chapter 49, we delve further

into existence propositions for critical points and their applications. In

particular, we deal with a general topological existence principle for saddle

points—the so-called Unking principle.

The justification of the Lagrange multiplier method for general situations

is an important concern in Part III. In this connection, compare Chapters

43, 47, 48, and 50.

The saddle point condition of the Kuhn-Tucker theory for convex

optimization problems (Sections 37.11, 47.10, 48.4, 50.1, and 50.2) and the

Pontrjagin maximum principle for control problems (Sections 37.21 and

48.6) are important contemporary extensions of the classical Lagrange

multiplier rule for problems with side conditions that are not necessarily

smooth.

References to the Literature

Sharp Lagrange multiplier rules in R": Hestenes (1966, M); Boltjanskii

(1976, M).

20

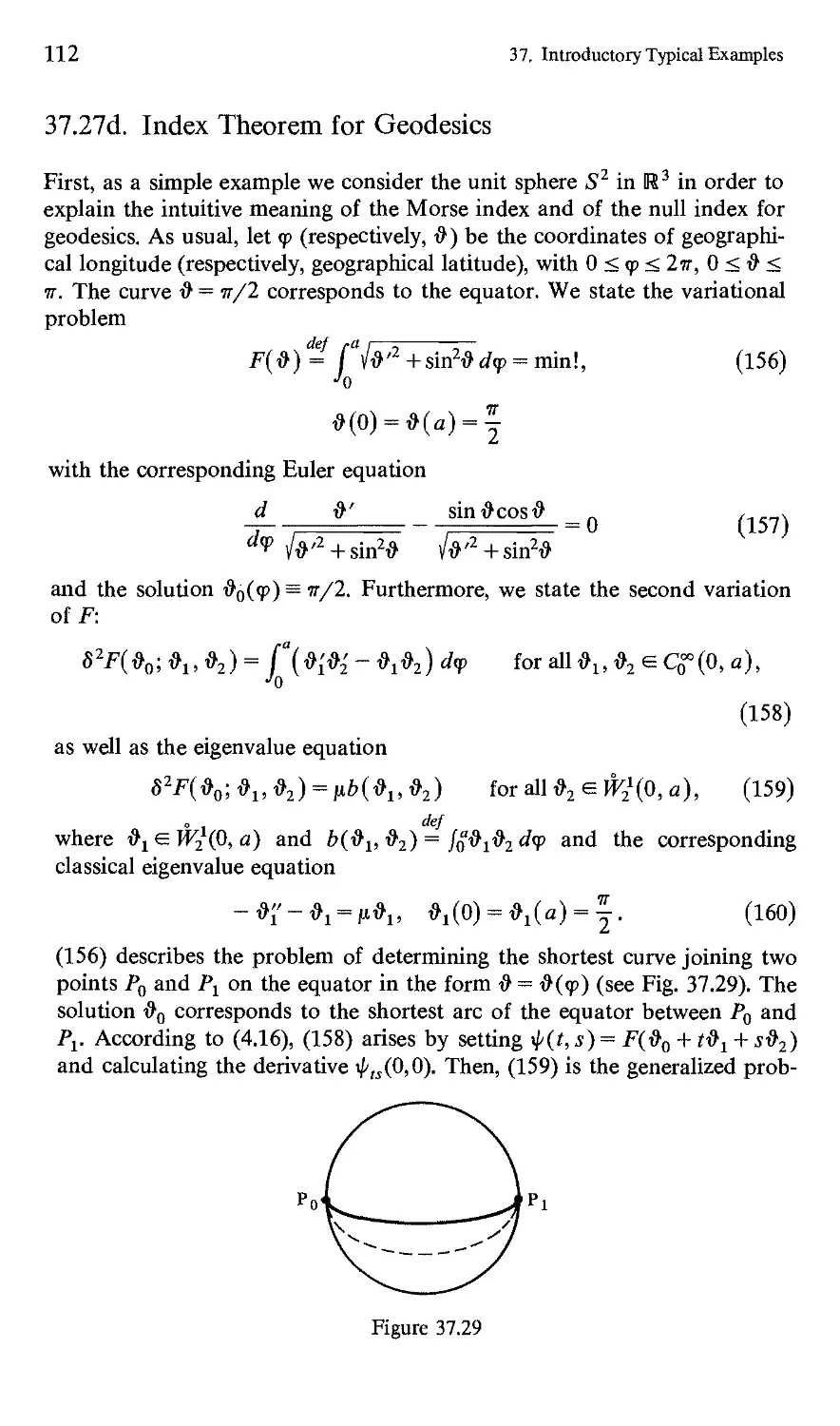

37. Introductory Typical Examples

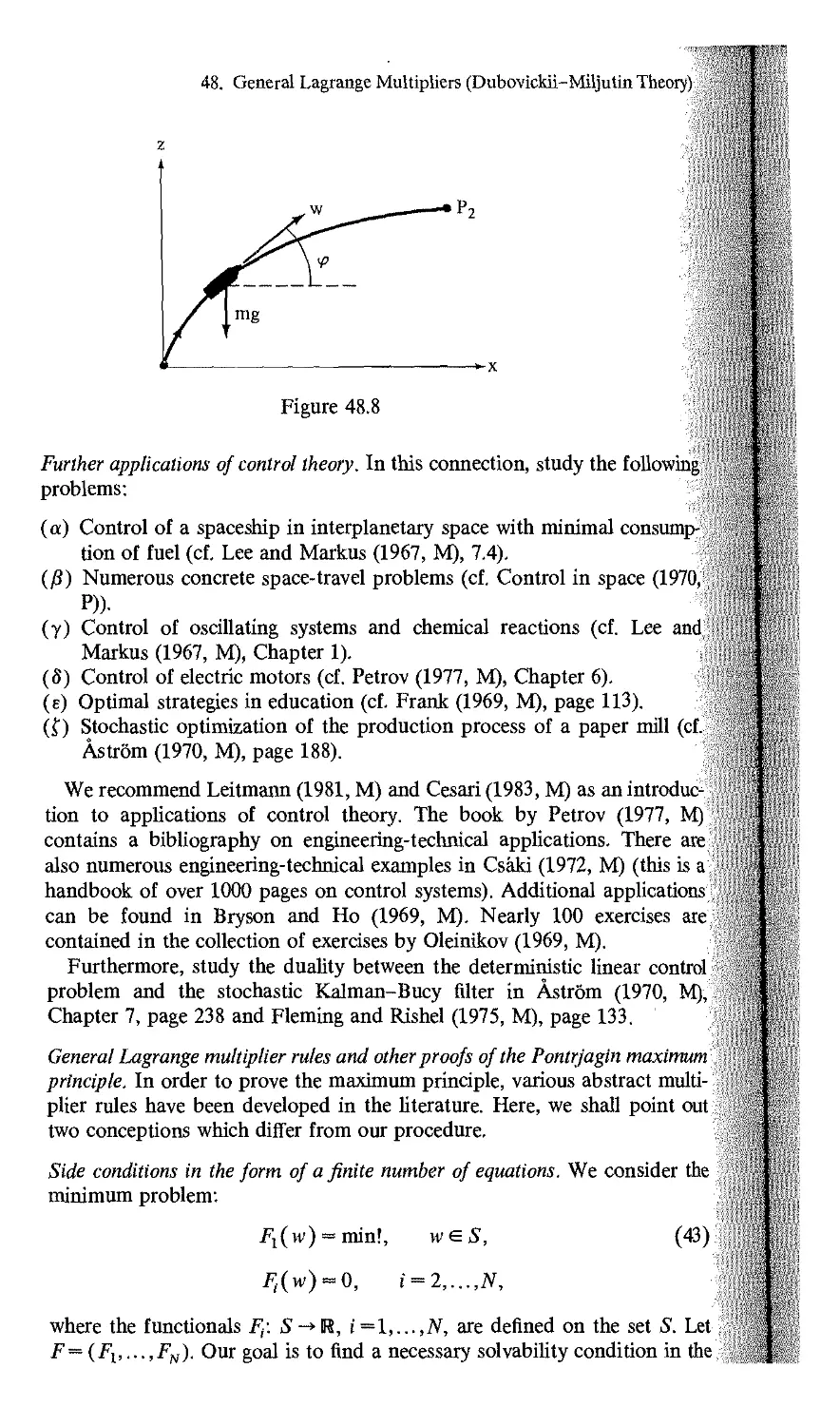

37.4. One-Dimensional Classical Variational Problems

and Ordinary Differential Equations, Legendre

Transformations, the Hamilton-Jacobi

Differential Equation, and the Classical

Maximum Principle

This section is of central significance for a deep understanding of many

assertions here in Part III. We present the results of the classical calculus of

variations in such a way that the reader will later see the connections with

convex analysis and control theory very clearly. The Hamilton-Jacobi

formalism is the focal point—this formalism is generalized in many ways in

the later chapters.

(a) Generalization of the canonical equations and of the classical maximum

principle: Pontrjagin's maximum principle and control problems.

(fl) Generalization of the Hamilton-Jacobi differential equation: Bellman's

principle of dynamic optimization in control theory, Bellman's

differential equation, and duality theory for nonconvex problems.

(•y) Generalization of the Legendre transformation: conjugate functional

in convex analysis and duality theory.

(5) Generalization of the Hamilton-Jacobi action function S: duality by

means of the stability of perturbed problems and the ^-functional.

The Hamilton-Jacobi theory represents a general framework for the

mathematical description of the propagation of actions in nature and the

optimal modelling of control processes in economics and technology. In

the Problems in Chapter 40, we point out a number of deep physical and

mathematical connections: geometrical optics, characteristics, bicharacteris-

tics and electromagnetic waves, hyperbolic partial differential equations,

Huygens' principle, diffraction theory, asymptotic expansions and the

Maslov index, Fourier integral operators, symplectic geometry, quasiclassi-

cal asymptotic expansions in quantum mechanics, the Feynman integral in

quantum mechanics and its connection with classical mechanics, integrable

canonical systems and perturbation theory in celestial mechanics, infinite-

dimensional canonical equations and nonlinear wave equations, etc. In Part

V we delve into the connection between classical mechanics, statistical

physics, and ergodic theory and explain the derivation of the fundamental

equations of mathematical physics on the basis of variational principles as

well as the meaning of symmetry principles and Lie groups in order to

obtain conservation quantities, similarity assertions, and gauge field

theories, which have achieved a basic significance in elementary particle physics.

This presentation, which is far from complete, should nonetheless facilitate

a feeling for the focal position of the Hamilton-Jacobi theory.